US Iran Peace Deal: Inflation Impact on Rate Cuts in 2026

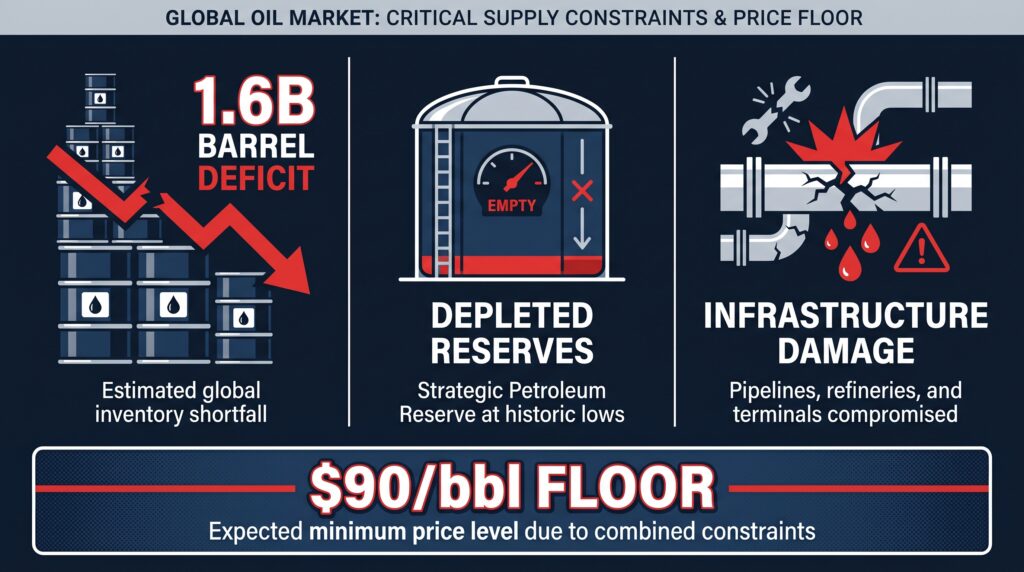

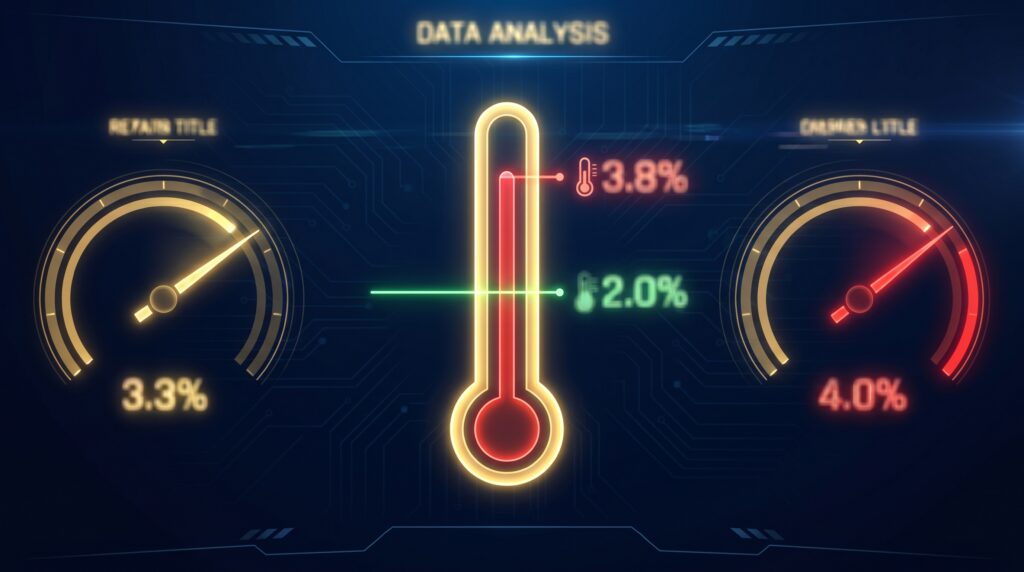

The 30-Second Sip: A 60-day US-Iran ceasefire has reopened Strait of Hormuz shipping lanes and sent a brief wave of relief through global equity markets. But the true US Iran peace deal inflation impact is far more complicated than the headlines suggest. The global oil market faces a structural deficit of 1.6 billion barrels that a diplomatic pause cannot replenish. PCE inflation sits at 3.8% — nearly double the Federal Reserve’s 2% target — with Core PCE accelerating to 3.3%.

Energy analysts do not expect crude to fall below $90 per barrel even if normal flows resume. And the 2-year US Treasury yield, locked at 4.0%, is already pricing in the possibility of fresh rate hikes rather than cuts. The ceasefire is logistically useful. It is not a macroeconomic cure.

Geopolitics and personal wealth management often feel like they belong in entirely separate conversations. For an investor tracking monthly index fund allocations or evaluating a fixed-income position, a diplomatic breakthrough in the Persian Gulf can seem like distant noise.

But the global financial ecosystem is deeply interconnected. The US Iran peace deal inflation impact flows directly from a maritime chokepoint in West Asia to the mortgage rate on a home in London, the yield on a Treasury bill in New York, and the valuation of an equity portfolio in Tokyo. As we advance through mid-2026, this is the defining question for global portfolio managers: will the proposed diplomatic breakthrough rescue markets from sticky inflation, or is the current optimism entirely premature?

Reports confirming that US and Iranian officials agreed to extend an ongoing ceasefire by 60 days and reopen Strait of Hormuz shipping lanes initially sent crude futures down more than 2% and equity indices ticking upward across major exchanges. But behind closed doors, central bankers at the Federal Reserve, the European Central Bank, and other major monetary authorities are striking a uniformly cautious tone.

The consensus among top economists is clear: do not expect a rapid monetary policy pivot. The structural damage to global energy supplies, and the stickiness of core inflation that damage has produced, means the era of elevated interest rates is far from over. Understanding why requires looking past the diplomatic headline and into the mechanics of what a ceasefire actually achieves — and what it completely fails to fix.

The Anatomy of the Deal: Optimism vs Structural Reality

To understand why central banks are refusing to celebrate the US Iran peace deal inflation impact with rate cuts, we must examine precisely what this diplomatic agreement achieves — and what it does not.

The cornerstone of current market optimism is the potential reopening of the Strait of Hormuz — the 33-kilometre-wide chokepoint that handles roughly one-fifth of the world’s total petroleum consumption daily. When the conflict erupted three months ago, partial closures and heightened security risk sent shipping insurance premiums sharply higher and forced supertankers onto longer, more expensive routes around Africa. A 60-day ceasefire extension and renewed shipping lane access would undeniably provide near-term supply chain relief.

However, investment bank ING noted in a May 2026 research note that geopolitical headlines regarding Hormuz reopening have become a recurring, cyclical pattern over recent months — yet the underlying economic fundamentals have not shifted with each optimistic announcement. Central banks do not formulate multi-year monetary policies based on volatile, short-term diplomatic headlines. They look at hard structural data. And the structural data for global energy markets tells a more worrying story than the ceasefire covers.

Why Energy Prices Have a Structural Floor

Even under a best-case scenario — a comprehensive peace treaty signed tomorrow — energy analysts do not expect crude prices to fall back to pre-war baselines. There are three compounding structural reasons why a floor of approximately $90 per barrel has been placed beneath global oil prices:

Reason 1 — The Inventory Deficit: The global oil market has been operating at a significant deficit since the outbreak of hostilities. Research from energy teams at major global banks estimates the market will be left short by upwards of 1.6 billion barrels when the dust settles. This missing supply cannot be replenished by reopening a shipping lane. It requires months of sustained production, not a diplomatic signature.

Reason 2 — Strategic Reserve Rebuilding: Major consuming nations — most notably the United States — have aggressively drawn down their Strategic Petroleum Reserves (SPR) over the past several years to artificially cap retail fuel prices. With global inventories now at historically low levels, any prolonged dip in crude prices will immediately trigger institutional buying as sovereign governments rush to restock emergency reserves. This structural buying behaviour acts as a price floor that absorbs downward pressure before it can meaningfully reach consumers.

Reason 3 — Damaged Production Infrastructure: Three months of conflict and heightened security threats have disrupted maintenance schedules and damaged extraction and transit infrastructure across the Middle East. Restoring oil flows to anywhere near normal capacity requires months of capital expenditure and engineering work that cannot be accelerated by a ceasefire announcement.

The Analyst Consensus: Due to these compounding structural realities, energy analysts at major global institutions do not expect crude prices to dip below $90 per barrel this year, even if normal flows resume in full. The floor is structural, not sentimental.

The Transmission Chain: How $90 Oil Reaches Interest Rates

How exactly does a structural crude floor translate into monetary policy decisions by central banks — and why does that matter to a global investor?

The relationship between an energy shock and benchmark interest rates follows a multi-step transmission chain that most investors only understand after it has already affected their portfolio:

Step 1 — The First-Round Effect: Elevated oil prices directly raise fuel costs at the pump and increase energy bills for businesses. Central banks can typically choose to “look through” this temporary shock, assuming it will fade with the geopolitical trigger.

Step 2 — The Mutation into Second-Round Effects: When oil stays high for months rather than weeks, the shock mutates. Higher fuel costs make it more expensive to transport goods, manufacture electronics, and run chemical plants. Companies begin embedding these permanently higher input costs into retail prices. Workers, realising their cost of living has jumped, negotiate for higher wages. Inflation stops being an energy story and becomes a structural services story.

Step 3 — Core Inflation Stickiness: Once higher energy costs imbed themselves into corporate pricing strategies and wage negotiations, inflation becomes sticky and persistent. Central banks cannot “look through” a structural shift — they must respond.

Step 4 — The Rate Hike Response: To combat structural stickiness, central banks maintain — or raise — benchmark interest rates to deliberately cool economic demand. The result: higher borrowing costs for businesses and households, delayed investment, slower economic growth.

This chain explains precisely why the US Iran peace deal inflation impact has not translated into rate cut expectations, even as oil futures briefly eased on the ceasefire news.

The Macroeconomic Data Behind the US Iran Peace Deal Inflation Impact

The hard numbers coming out of the developed world confirm that second-round effects are already manifesting. The Federal Reserve’s preferred inflation metric — the Personal Consumption Expenditures (PCE) Price Index — tells a stark story:

|

Economic Indicator |

Latest Value |

Previous Period |

Policy Target |

|---|---|---|---|

|

Headline PCE Inflation |

3.8% (April 2026) |

3.5% (March 2026) |

2.0% |

|

Core PCE Inflation |

3.3% (April 2026) |

3.2% (March 2026) |

2.0% |

|

New York Fed Inflation Gauge |

4.0% (April 2026) |

3.5% (March 2026) |

N/A |

|

2-Year US Treasury Yield |

4.0% |

~3.75% (prior) |

N/A |

Source: Federal Reserve / Bureau of Economic Analysis / NY Fed, April–May 2026

The fact that Core PCE — which deliberately excludes volatile food and energy components — ticked up to 3.3% is the most important signal in this table. Core inflation rising means that elevated energy costs have already seeped beyond the pump and into the broader services economy. The US Iran peace deal inflation impact is not just an energy headline; it is now embedded in the structural core. Federal Reserve PCE data releases.

This reality has caused a dramatic shift in tone among central bank policymakers. Fed Governor Lisa Cook stated openly that she is closely watching whether companies are embedding higher energy costs into consumer prices — and is “prepared to raise rates” if the expected disinflation does not appear in a timely manner. Kansas City Fed President Jeffrey Schmid echoed this aggressive stance, noting that looking through energy shocks is no longer viable and the central bank may need to use its balance sheet to actively restrict monetary conditions.

Minneapolis Fed President Neel Kashkari noted it is premature to rule out additional monetary tightening, emphasising that the risk of inflation continuing to climb demands active vigilance.

Even the bond market — historically more accurate than equity markets at predicting the economic future — is signalling trouble. The 2-year US Treasury yield, locked at 4.0%, is pricing in a distinct possibility of a 25-basis-point rate hike rather than any near-term cut.

Two Investors, One Ceasefire: Different Outcomes

This is a fictional educational scenario. Not investment advice. All figures are illustrative only.

Sarah and Marcus — both experienced global retail investors — heard the same ceasefire headline on the same morning in May 2026.

Sarah’s response: Sarah interprets the Strait of Hormuz reopening as a signal that inflation will ease rapidly and rate cuts are imminent. She rotates a significant portion of her fixed-income holdings from short-duration Treasury bills into long-duration government bond funds to capture the anticipated price appreciation that rate cuts would deliver.

Within three weeks, Core PCE data confirms inflation is still rising. The Fed signals rates will remain elevated through year-end. Long-duration bond fund NAVs drop as yields tick higher. Sarah’s rotation has produced an immediate capital loss on paper — in the exact instruments she believed would benefit from the policy pivot she expected.

Marcus’s response: Marcus reads the same headline but focuses on the structural data: 1.6 billion barrel deficit, depleted SPR levels, damaged infrastructure, Core PCE still accelerating. He maintains his short-duration debt positions to capture current high yields without duration risk. He retains a modest allocation to gold as an inflation hedge and holds cash for future deployment.

When the same Core PCE data drops, Marcus’s short-duration instruments continue performing near face value. His gold allocation registers a small gain on the inflation print. His cash is available to redeploy if equity prices correct on the rate surprise.

The difference between Sarah and Marcus was not market access, intelligence, or investment horizon. It was the discipline to look past the headline and read the structural mechanism underneath it.

How Market Participants Navigate a Higher-for-Longer Environment

Note: This section describes historical market participant behaviour for educational purposes only.

In an environment where global interest rates are structurally elevated and energy markets face compounding supply constraints, the US Iran peace deal inflation impact on portfolio management has historically been approached through several principles:

Fixed Income and Cash Management: In higher-for-longer rate environments, market participants have historically favoured short-to-medium duration fixed-income instruments — such as short-term Treasury bills and high-yield savings instruments — over long-duration bonds. The logic: short-duration instruments mature quickly, allowing reinvestment into higher-yielding instruments without suffering the capital loss that rising rates inflict on long-duration portfolios. Locking in current high yields before the eventual rate cycle turn has historically been the dominant institutional approach during this phase.

Equity Portfolio Positioning: In high interest-rate regimes, analysts have consistently noted that the cost of servicing capital creates a drag on heavily leveraged companies. Historical studies of rate-elevated cycles show that companies with strong balance sheets, high internal cash generation, and low debt-to-equity ratios tend to outperform peers with heavy refinancing requirements. Additionally, companies with genuine pricing power — the ability to pass input cost inflation on to customers without losing market share — have historically demonstrated more resilient earnings in persistent inflation environments.

Commodity and Alternative Allocations: Gold has historically been observed as an outperformer in environments characterised by persistent inflation, geopolitical friction, and currency volatility. During the 1970s stagflation cycle and subsequent commodity shocks, gold acted as a structural portfolio anchor for investors navigating prolonged above-target inflation regimes — a pattern that portfolio historians have documented across multiple cycles.

The Gyani Turtle Verdict

The US Iran peace deal inflation impact is being both overestimated and underestimated simultaneously — and in opposite directions.

Markets are overestimating the ceasefire’s ability to resolve structural energy supply problems that took three months to create. A 60-day diplomatic pause does not replenish 1.6 billion barrels of missing crude, restock depleted strategic reserves, or repair damaged production infrastructure across the Gulf. The structural floor beneath oil prices at approximately $90 per barrel is a market reality, not a negotiating position.

Markets are simultaneously underestimating the stickiness of the inflation that three months of elevated energy costs have already injected into the services economy. When Core PCE — which excludes energy entirely — still accelerated to 3.3% in April 2026, it confirmed that the energy shock has already mutated into the broader cost structure. Central banks do not respond to diplomatic headlines; they respond to PCE prints.

Here is how to think about this environment:

- The ceasefire is logistics, not macroeconomics — a temporary supply chain relief that does not change the inflation trajectory

- The energy structural floor matters more than the headline price — $90/bbl is not the same market as $70/bbl for corporate margins and consumer budgets

- Core PCE is the signal to watch — not oil futures, not ceasefire timelines

- The 2-year Treasury at 4.0% is the market’s honest assessment — it is pricing in holding, not cutting

- Duration in fixed income is the specific risk to understand — long-duration bonds lose value in a higher-for-longer environment in a mathematically predictable way

- Patience in equities is rewarded — systematic investment through elevated-rate cycles has historically delivered, provided the underlying companies carry manageable debt

The peace deal is welcome. It reduces near-term supply chain friction. It is not a policy pivot signal. The investors who treat it as one will likely face the same surprise as every previous Hormuz ceasefire optimist of the past six months.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Also read:

- Is Your SIP Nifty IT Safe? 5 Truths About AI and India’s IT Stocks in 2026

- India’s $180B Data Center Boom: The 2026 AI Investment Guide

- Market Volatility: 3 Reasons Indian Investors Shouldn’t Panic

- How to Start Investing in India as a Beginner

⚠️ EDUCATIONAL CONTENT ONLY

Gyani Turtle is NOT a SEBI-registered Investment Adviser (RIA) or Research Analyst (RA), and is not a licensed financial adviser in any jurisdiction globally. This article is written for general financial education and awareness only. Nothing in this article constitutes personalised investment advice, a solicitation, or a recommendation to buy or sell any security, fund, or financial instrument in any market.

Please consult a SEBI-registered Investment Adviser, AMFI-registered Mutual Fund Distributor, or a licensed financial professional in your jurisdiction before making any investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.

4 Comments