Start Investing in India — Best Essential Beginner’s Guide 2026 | Gyani Turtle

To start investing in India as a beginner, open a free Demat account on Groww or Zerodha, build a 6-month emergency fund first, then start a monthly SIP in a Nifty 50 index fund with as little as ₹500. Clear high-interest debt and get basic insurance before investing any money in the market.

You’ve been meaning to start investing for a while now.

This guide on how to start investing in India is designed

for complete beginners — no jargon, no hype.

Maybe you saw a friend’s portfolio screenshot. Maybe a YouTube ad about making money in the stock market finally pushed you to search. Maybe you just got your first salary hike and thought — there has to be something smarter to do with this money than let it sit in a savings account earning 3%.

Whatever brought you here — welcome. If you’ve been searching for how to start investing in India, you’re in the right place.

This guide will not tell you about “hot stocks” or “multibagger opportunities.” It will not promise you 10x returns in 6 months. What it will do is give you the honest, step-by-step foundation that most Indians never get — the kind of foundation that builds real, lasting wealth quietly over decades.

Let’s start from the very beginning.

Why You Cannot Afford to Not Invest in India

Let’s start with an uncomfortable truth.

Your savings account is losing you money.

Not in the obvious way where your balance decreases — but in the silent, invisible way that inflation works. With inflation hovering around 6–7%, a traditional fixed deposit at 7% is barely keeping your head above water after taxes. Your money is technically growing. But its purchasing power — what it can actually buy you — is shrinking every year.

Here’s what that means in practical terms:

If a bag of groceries costs ₹3,000 today, it’ll cost roughly ₹5,370 in 10 years at 6% inflation. The ₹3,000 sitting in your savings account earning 3% interest will only grow to about ₹4,031 in the same period. That’s a gap of over ₹1,300 — on just one grocery bill.

Multiply that across every expense in your life. That’s the cost of not investing.

The Indian stock market has given an average return of around 12–14% over the long term. The Sensex has grown from 1,000 in 1990 to over 82,000 in 2026 — an 82x return across 35 years. That’s the power of equity compounding working quietly in the background.

Investing is not gambling. It’s not speculation. For a patient, long-term investor — it’s the single most reliable way to make your money grow faster than inflation.

Step 1 — Build Your Financial Foundation First

Before you invest a single rupee, you need to do three things. Skip these and you’ll be forced to sell your investments at the worst possible time.

1. Clear High-Interest Debt First

If you have credit card debt, personal loans, or any debt costing more than 12% annual interest — pay that off before investing.

Here’s why: If your credit card charges 36% per year and your equity investment returns 12% per year, you’re still losing 24% net. Paying off debt is a guaranteed, risk-free return.

2. Build an Emergency Fund

Keep 6–12 months of expenses tucked away as an emergency fund in a high-interest savings account or a liquid mutual fund — not invested in equity. If you work in the private sector, especially in a field being disrupted by technology or AI-driven hiring shifts, lean toward the 12-month side. Job markets in 2026 are moving faster than ever — your financial cushion should reflect that reality.

This is your financial airbag. It ensures that when life throws a curveball — job loss, medical emergency, urgent repair — you don’t have to crack open your investments at a loss to cover it.

3. Get Basic Insurance Coverage

Before investing for wealth, protect against wealth destruction. A term insurance plan and a health insurance plan are non-negotiable. If a medical emergency can wipe out your entire portfolio, you haven’t built wealth — you’ve built an emergency fund with extra steps.

Only after these three foundations are in place should you move to Step 2.

Step 2 — Where Can You Invest When Starting in India?

India gives you many places to put your money. Here’s a plain-English breakdown of the main options:

Equity (Stocks and Mutual Funds)

You buy a small ownership stake in real companies. When the company grows, your investment grows. This is the highest-returning asset class over the long term — but also the most volatile in the short term. Best for goals that are 5+ years away.

Debt (Fixed Deposits, Bonds, Debt Mutual Funds)

You lend money to a bank, company, or government and earn fixed interest. Lower returns than equity, but stable and predictable. Best for short-term goals or as a stability cushion in your portfolio.

Gold

A traditional Indian store of value. Protects against currency depreciation and adds portfolio diversification. Does not generate income like a business does, but acts as a hedge during economic uncertainty. Best held as 5–10% of your portfolio, not as the main investment.

Real Estate

High capital requirement, low liquidity, and significant transaction costs make it unsuitable as a beginner’s first investment. If you’re just starting out, skip this for now.

PPF and NPS

Government-backed, tax-efficient, and safe. PPF (Public Provident Fund) currently earns around 7.3% with full tax exemption under Section 80C (Note: 80C benefits apply only under the Old Tax Regime — the New Tax Regime, which is now the default for most Indians, does not offer Section 80C deductions). NPS (National Pension System) is powerful for retirement planning with additional tax benefits. Both are excellent for the debt/stability portion of your portfolio.

For a beginner in 2026, the sweet spot is equity mutual funds (specifically index funds) combined with PPF for stability.** Everything else can be added later as your knowledge grows.

Step 3 — How to Start Investing in India: Open a Demat Account First

To invest in stocks or ETFs directly in India, you need three accounts linked together:

- Bank Account — Where your money lives (you already have this)

- Demat Account — The digital locker where your shares are stored electronically

- Trading Account — The platform where you place buy and sell orders

Modern stockbrokers open your trading and demat accounts simultaneously in about 15 minutes. You don’t need to visit a branch or sign 40 pages of documents.

Which Broker Should You Choose?

You have two options: full-service brokers like HDFC Securities or ICICI Direct, and discount brokers like Zerodha or Groww. Unless you want to pay high fees for mediocre stock tips, go with a discount broker. They charge zero commission for holding stocks long-term and have clean, easy-to-use apps.

For most beginners, we recommend:

Groww — Now India’s largest broker by total active clients as of early 2026. Simplest app experience for absolute beginners. Great for mutual funds and increasingly good for stocks.

Zerodha Kite — Still India’s most trusted broker by trading volume. Reliable, zero delivery brokerage, and powerful interface. Slight learning curve but worth it for serious investors.

Angel One — Good alternative with solid research tools built in.

All three are SEBI-registered, reliable, and beginner-friendly.

Documents you’ll need:

PAN card

Aadhaar card

Bank account details (cancelled cheque or passbook)

A selfie or short video for KYC verification

The entire process is online and takes 1–2 business days to activate after submission.

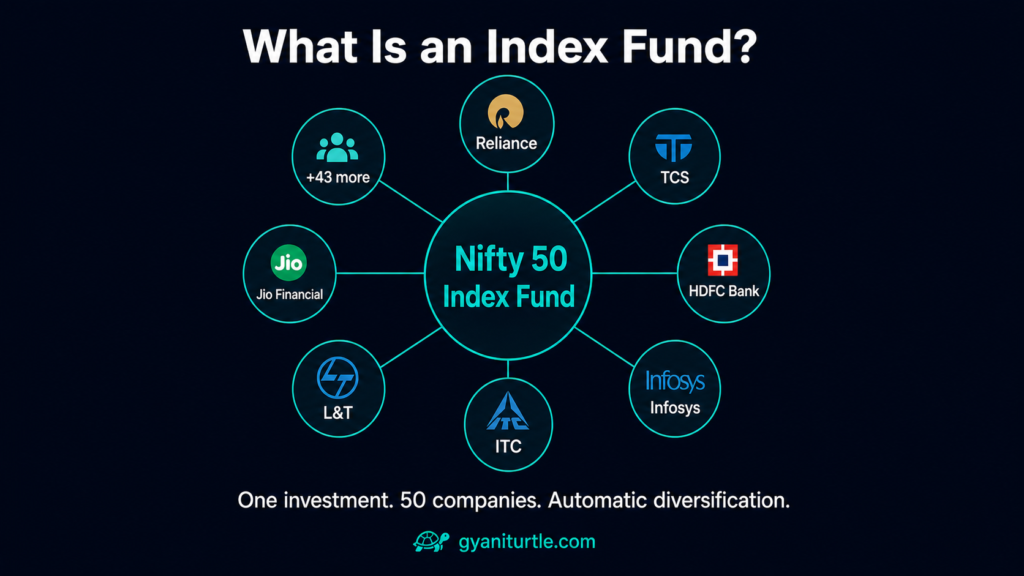

Step 4 — Make Your First Investment: Index Funds

If you are a total beginner, forget about analysing individual companies for a minute. Your first investment should be an index fund or an ETF. Instead of trying to pick the winning horse, just buy the entire racetrack.

Here’s what that means in practice.

The Nifty 50 is a basket of the 50 largest, most successful companies listed on the NSE — Reliance, TCS, HDFC Bank, Infosys, ITC, and 45 others. When you buy a Nifty 50 index fund, your money is automatically spread across all 50 companies. If one company has a bad year, the other 49 balance it out. If a company becomes too small, it gets replaced automatically by a stronger one.

It’s essentially a self-cleaning, self-rebalancing portfolio — managed by the market itself.

Best Nifty 50 Index Funds for Beginners (2026)

UTI Nifty 50 Index Fund — One of the lowest expense ratios in the category

HDFC Index Fund – Nifty 50 Plan — Reliable, well-managed, popular

SBI Nifty Index Fund — Backed by India’s largest public sector bank

All three track the same Nifty 50 index. The primary difference is the expense ratio — choose the one with the lowest cost, as fees compound just as powerfully as returns do over time.

⚠️ Important Note: Before investing in any mutual fund, verify its current status on your broker’s platform. Some international funds and certain index funds are periodically suspended for fresh lumpsum investments due to SEBI’s regulatory limits. Always check availability before attempting to invest.

Step 5 — Start a SIP (Systematic Investment Plan)

A SIP is the most powerful habit a beginner investor can build.

Instead of investing a lump sum once and hoping for the right timing, a SIP automatically deducts a fixed amount from your bank account every month and invests it in your chosen fund. The magic is in the consistency — not the amount.

You can start a SIP with as little as ₹500 or ₹1,000 per month in 2026. That’s less than a meal at a mid-range restaurant. But over 20 years at a 12% average return, ₹5,000 per month becomes approximately ₹49 lakh. The same ₹5,000 per month in a savings account at 3% becomes about ₹16 lakh. The difference? ₹33 lakh — generated purely by being in the right asset class consistently.

The SIP Step-Up Strategy

One powerful strategy many investors ignore is the SIP step-up. Whenever your salary increases, increase your SIP amount. Even a 5–10% increase every year can dramatically improve your final corpus.

If you start at ₹5,000/month today and increase your SIP by just 10% every year, in 20 years you’d have over ₹1 crore — without any change in market conditions. That’s the step-up effect.

Step 6 — Build Your First Portfolio (Keep It Simple)

Once you’re comfortable with your index fund SIP running for 3–6 months, you can think about building a simple portfolio around it.

A beginner portfolio doesn’t need to be complex. Here’s a framework:

Conservative Beginner (Lower risk tolerance):

- 60% — Nifty 50 Index Fund (SIP)

- 30% — PPF (monthly contribution)

- 10% — Gold (Sovereign Gold Bonds or Gold ETF)

Moderate Beginner (Medium risk tolerance):

- 70% — Nifty 50 Index Fund (SIP)

- 15% — Nifty Next 50 or Midcap 150 Index Fund

- 10% — PPF

- 5% — Gold ETF

Growth-Oriented Beginner (Higher risk tolerance, long time horizon):

- 80% — Nifty 50 + Nifty Next 50 Index Funds

- 10% — International Index Fund (check SEBI availability)

- 10% — Gold ETF or Sovereign Gold Bond

Notice what’s missing from all three? Individual stock picks. That comes later — after you’ve spent at least 1–2 years understanding how markets move, how you personally react to volatility, and what your real risk tolerance is (not what you think it is until your portfolio drops 20%).

Step 7 — The Investor Psychology Crash Course

Technical knowledge is only 20% of investing. The other 80% is managing your own mind.

Most people don’t lose money because markets are bad. They lose money because of poor decisions. Here are the five biggest mistakes beginners make — and how to avoid them:

Mistake 1: Checking Your Portfolio Every Day

The stock market moves daily. Your investments are for 10–20 years. Checking your portfolio every day is like weighing yourself every hour while dieting — you’ll drive yourself crazy and make irrational decisions based on noise. Check your portfolio once a quarter.

Mistake 2: Panic Selling During Market Falls

You will wake up one day, check your app, and see your portfolio down by 20%. It feels terrible. Your stomach will drop. But this is a feature, not a bug. If you don’t sell, you haven’t lost a single rupee. Market corrections are temporary. Panic selling makes them permanent.

Mistake 3: Following Social Media Tips

A random person on Instagram showing you a stock tip has either already bought it and is trying to push the price up, or is genuinely clueless. Neither helps you. Stick to your index fund SIP and ignore the noise.

Mistake 4: Waiting for the “Right Time” to Invest

There is no right time. The best time was 10 years ago. The second best time is today. Time in the market always beats timing the market.

Mistake 5: Starting Too Complex

Beginners often buy 8 different mutual funds thinking more funds means more diversification. In reality, five large-cap funds tracking the same index is not diversification — it’s duplication with extra paperwork. Start with one or two funds. Add complexity only when you understand what and why.

Your Complete Beginner Action Plan to Start

Investing in India

Here’s exactly what to do, in order, starting today:

Week 1:

- Calculate your monthly expenses

- Set aside 6 months of expenses as emergency fund goal

- Get a term insurance quote (policybazaar.com for comparison)

Week 2:

- Open a Demat account on Zerodha or Groww

- Complete KYC with PAN + Aadhaar

- Wait for account activation (1–2 days)

Week 3:

- Search for “UTI Nifty 50 Index Fund” or “HDFC Nifty 50 Index Fund” on your broker’s platform

- Set up a monthly SIP for whatever amount doesn’t stress your budget (₹500 is fine)

- Link it to your bank account and confirm the first deduction date

You’ve now officially begun your journey of investing

in India.

Month 2 onwards:

- Do NOT check your portfolio more than once a month

- Spend 30 minutes reading one quality article about investing each week

- Gradually increase your SIP amount as your income grows

- Revisit your portfolio allocation once every 6 months — not more

The Bottom Line

Investing in India in 2026 has never been more accessible. You can start with ₹500, open an account in 15 minutes, and be invested in 50 of India’s best companies by the end of this week.

The real barrier isn’t money. It isn’t knowledge. It’s starting.

The Indian middle class has a peculiar habit of hoarding savings in FDs and gold while watching inflation quietly erode purchasing power. Meanwhile, the stock market — patient, boring, and completely indifferent to your anxiety — keeps compounding for those who simply stay invested.

How to start investing in India in 2026 has never been easier to figure out — the barrier isn’t money or knowledge, it’s starting.

You don’t need to be smart. You don’t need perfect timing. You don’t need an MBA.

You need to start, stay consistent, and resist the very human urge to do something dramatic every time the market moves.

The turtle wins the race. Every time.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Ready to open your first investment account? Drop your questions in the comments below — we read every single one.

Ready to grow your money?

See How Much Your SIP Can Grow

Use our free SIP Calculator — enter your monthly amount and see the power of compounding over 10, 20, or 30 years.

Try the SIP Calculator →Disclaimer: This article is for educational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks. The investment options, platforms, and returns mentioned are for illustrative purposes only. Please read all scheme-related documents carefully and consult a SEBI-registered investment advisor before making any investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.

5 Comments