SGB vs Gold ETF vs Electronic Gold Receipt: The Only Gold Guide You Need in 2026

Gold is India’s oldest obsession. And in 2026, with oil touching $126 a barrel and the Rupee under sustained pressure, that obsession is costing every Indian more than they realize. Here is the uncomfortable truth: the problem is not that you own gold. The problem is how you own it.

SGB vs Gold ETF vs EGR

Every gram of physical gold India imports is paid for in US Dollars — dollars the RBI must defend, dollars that weaken the Rupee, dollars that come back to you as higher EMIs, costlier vegetables, and an inflation rate that quietly erodes everything you saved. The good news is that in 2026, you have three intelligent alternatives to the physical gold sitting in a locker. Sovereign Gold Bonds (SGBs), Gold ETFs, and the relatively new Electronic Gold Receipt (EGR) — each with a different risk profile, return structure, and tax treatment. This post breaks all three down completely, so you can stop owning gold the wrong way.

🐢 TURTLE’S RAPID RESPONSE

- Long-term investor (5+ years)? SGB — zero tax at maturity + 2.5% annual interest

- Need flexibility? Gold ETF — buy and sell any day, low cost

- Want physical delivery option? EGR — exchange-traded with optional physical withdrawal

- Physical gold for a wedding? Use old-for-new exchange — do not import fresh gold

- Never do: Buy physical gold bars as an “investment” in 2026

Why This Decision Matters More in 2026 Than Any Previous Year ?

The gold-Rupee connection is not abstract economics. Here is exactly how your physical gold purchase travels from your hands to your EMI statement:

Step 1 →

Oil hits $126/barrel. Global uncertainty spikes. Indian households panic-buy physical gold “for safety.”

Step 2 →

To meet this demand, India imports more gold — paying in US Dollars. India’s forex reserves have dropped from $728 billion to $691 billion in recent months.

Step 3 →

As India sells Rupees to buy Dollars for gold and oil imports, the Rupee depreciates sharply against the Dollar.

Step 4 →

A weaker Rupee makes everything else imported — electronics, chemicals, fertilisers — more expensive. Inflation rises.

Step 5 →

To defend the Rupee and control inflation, the RBI raises interest rates.

Step 6 →

Your home loan EMI jumps by ₹3,000–5,000 per month.

Step 7 →The Irony

The physical gold in your locker gained 10% in value. Your cost of living went up 20% because millions of people made the same purchase decision as you.

SGBs, Gold ETFs, and EGRs break this chain at Step 2 — they allow you to own gold without India importing a single additional gram.

The Three Options — What Each One Actually Is ?

Sovereign Gold Bond (SGB)

Issued by the RBI on behalf of the Government of India. When you buy an SGB, you are buying a government bond whose value is linked to the gold price. You earn 2.5% annual interest on your initial investment, paid semi-annually in cash. Hold it for 8 years to maturity and your capital gain is completely tax-free. SGBs are listed on stock exchanges but trading volumes are thin — treat this as a hold-to-maturity instrument.

Gold ETF

A mutual fund unit that tracks the price of 24-karat gold. Traded on NSE and BSE just like a stock — you can buy and sell any trading day at market price. No lock-in, no storage cost beyond the fund’s expense ratio (typically 0.5–1% per year). Capital gains taxed at 12.5% LTCG after 12 months. Best for investors who want gold exposure with full liquidity.

Electronic Gold Receipt (EGR)

The newest of the three. An EGR is a receipt issued against physical gold deposited in a SEBI-regulated vault in India. You can buy EGRs in denominations as small as 100mg (0.1 gram) on NSE or BSE — making it the most accessible of the three. The unique feature: you can convert your EGR back into physical gold by withdrawing from the vault (3% GST applies only at this point). SEBI mandates that every EGR is backed 1:1 by 999-purity gold in a domestic vault — no dollar drain involved.

The Head-to-Head Comparison

|

Feature |

SGB |

Gold ETF |

EGR |

Physical Gold |

|---|---|---|---|---|

|

Returns |

Gold price + 2.5% interest |

Gold price − expense ratio |

Gold price − vaulting fee |

Gold price − storage + making charges |

|

Liquidity |

Low — thin exchange volumes |

Very High — T+1 settlement |

High — exchange traded |

Medium — jeweller dependent |

|

Tax at exit |

0% at maturity |

12.5% LTCG |

12.5% LTCG |

12.5% LTCG |

|

Minimum investment |

1 gram |

~₹100 (via SIP) |

100mg |

Typically 1–2 grams |

|

Physical delivery? |

No |

No |

Yes — optional |

Yes |

|

GST on purchase |

0% |

0% |

0%(3% only if converting to physical) |

3% |

|

Storage cost |

None |

0.5–1% expense ratio |

Minimal vaulting fee |

Locker rent ₹3,000–8,000/year |

|

Supports India’s forex? |

✅ Yes |

✅ Yes |

✅ Yes |

❌ No |

|

Best for |

Long-term wealth building |

Flexible SIP investing |

Tactical traders |

Jewellery / gifting only |

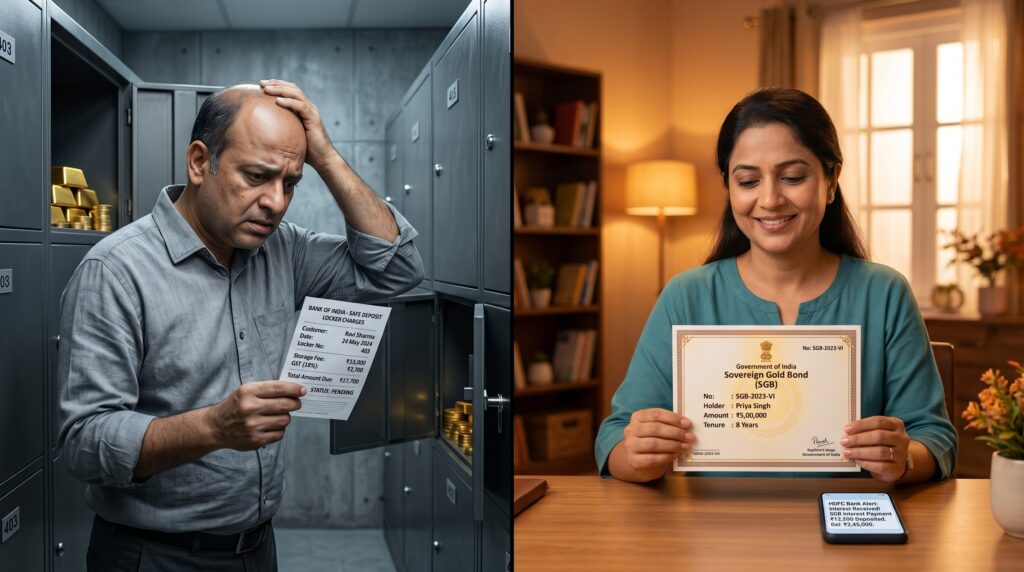

The Iyer Family: The Right Choice vs The Wrong Choice

The Iyer Family, Chennai. Monthly income: ₹1.4 lakh. Goal: Wedding savings by 2030.

The wrong choice — Mr. Iyer buys 100 grams of physical gold:

- Cost: ₹15.6 lakh + 3% GST = ₹46,800 upfront

- Locker rent: ₹4,000 per year = ₹16,000 over 4 years

- Making charges if converted to jewellery: 8–15%

- National impact: Approximately $18,500 in forex spent

- Tax on gains: 12.5% LTCG on profits

- Total invisible cost before any price movement: ₹62,800+

The right choice — Mrs. Iyer puts ₹15.6 lakh into SGBs:

- GST: Zero

- Locker rent: Zero

- Annual interest at 2.5%: ₹39,000 per year = ₹1.56 lakh over 4 years

- Capital gains tax at exit: Zero (maturity redemption)

- National impact: Zero forex spent

- Total advantage over physical gold: ₹1.56 lakh in interest + ₹46,800 GST saved + ₹16,000 locker saved = ₹2.19 lakh ahead before gold price movement

The gold price appreciation is identical in both cases. Every other variable favours the SGB.

Who Should Choose What ?

If you are a salaried investor with a 5+ year horizon:

SGB is your best option — full stop. The 2.5% annual interest is essentially free gold, the tax exemption at maturity is unmatched, and you are supporting India’s forex position. Open a new SGB window via your bank or RBI Retail Direct.

If you want to invest monthly via SIP:

Gold ETF. Set up a monthly SIP of even ₹500–1,000 in a Gold ETF through Zerodha, Groww, or any broker. You get rupee-cost averaging on gold without needing an SGB window to be open.

If you are a tactical investor or trader:

EGR. The exchange-traded nature with optional physical delivery gives you the most flexibility. Useful if you want to hold gold short-term and potentially take delivery for a specific occasion without paying import premiums.

If you are buying gold for a family wedding:

Use the old-for-new exchange programme at reputed jewellers. Do not import fresh gold. If you want to gift something meaningful, an SGB certificate is increasingly accepted as a sophisticated, thoughtful gift — and one that earns interest.

The Contrarian View — What the Skeptics Say

The case against paper gold deserves a fair hearing.

The systemic collapse argument:

Critics point out that in a true financial crisis, an EGR or ETF is a line of code in a Demat account. If the banking system collapses, your digital receipt is worthless.

The Counter:

if the Indian banking system collapses completely, the jewellery in your locker will not save you either. You will be trading for food, not fashion. Physical gold is a hedge against moderate uncertainty — not civilisational collapse.

The SGB liquidity trap:

SGBs are listed on exchanges, but secondary market volumes are genuinely thin. If you need to exit an SGB before maturity in an emergency, you may sell at a 3–5% discount to market price. This is a real limitation that most SGB evangelists understate.

The honest answer:

No single instrument is perfect. The right portfolio holds a combination — SGBs for the long-term core, Gold ETFs for the liquid layer, and zero physical gold beyond what you actually wear.

What SEBI and RBI Are Doing ?

RBI has been limiting SGB issuance windows — making them less frequent and more exclusive — to drive demand toward digital gold formats and reduce the pressure to launch new tranches that impact fiscal management.

SEBI has placed strict regulations on EGR vault managers, mandating that every EGR traded on NSE or BSE is backed 1:1 by 999-purity gold in a high-security domestic vault. This removes the counterparty risk that made earlier digital gold products (like app-based gold) controversial.

IMF has noted in recent assessments that India’s gold import dependency is a structural drag. The transition to EGRs is viewed as a positive sovereign move that keeps gold value circulating within the domestic financial system.

The Gyani Turtle Verdict

Gold is not the problem. Physical gold imports are.

SGBs win on pure financial mathematics — zero tax at maturity, 2.5% annual interest, zero storage cost, and full government backing. If you have a 5-year horizon and do not need the money, there is no rational argument for choosing physical gold over an SGB.

Gold ETFs win on flexibility — if you want liquidity, monthly SIPs, or the ability to exit at any time, they are the right tool.

EGRs win on innovation — the ability to own exchange-traded, vault-backed gold with optional physical delivery is genuinely new and worth understanding, particularly for investors who want the option to eventually take physical possession without paying import premiums.

The patient investor’s gold allocation for 2026:

- 60–70% in SGBs — long-term, tax-free core

- 20–30% in Gold ETFs — liquid layer for flexibility

- 0–10% in EGRs — tactical, if you want delivery optionality

- 0% in physical gold bars — unless it is jewellery you actually wear

Gold has preserved wealth for thousands of years. The form it takes in your portfolio should preserve it for the next twenty.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Also read:

- Is Nifty IT Safe to Invest in 2026? The AI Disruption Truth

- The White Collar Recession Nobody Is Talking About

- Start Investing in India — Best Essential Beginner’s Guide 2026

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before making investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.