Is the Next Fed Rate Hike Approaching? What Global Investors Should Watch Now

Fed rate hike 2026 is no longer a fringe scenario — and global investors who are still positioned for cuts may be carrying more risk than they realize.

That story now looks a lot less certain.

Inflation in the US has started heating up again, financial conditions are still looser than many expected, and some Fed officials are openly signaling that the fight against inflation may not be fully over. That raises an uncomfortable but important question for every investor watching global markets right now:

What if the Fed’s next move is not a cut — but a hike?

A renewed Fed rate hike is no longer a fringe scenario. For global investors, this shifting monetary landscape matters far beyond the United States. A more hawkish Federal Reserve can affect the dollar, bond yields, emerging market flows, equity valuations, and commodity prices across every major economy in the world.

Let’s break down exactly what is happening, why it matters, and what to watch next.

Why the Fed Rate Hike Debate Has Reopened

The biggest reason this conversation is back on the table is straightforward: inflation is proving harder to fully defeat than markets expected.

When inflation falls steadily toward its target, central banks can afford to be patient and let lower rates do their work over time. But when price pressures start rising again — especially after financial markets have already positioned for rate cuts — policymakers have no choice but to recalibrate. Fast.

That is exactly where we are heading into the second half of 2026.

Even though the Fed has kept rates unchanged for now, the tone of the internal policy debate has clearly shifted. The conversation has moved from asking when cuts begin to asking something far more unsettling for portfolios built on the old consensus: what if cuts are delayed indefinitely — or replaced by another hike?

That change in narrative alone is powerful enough to reprice assets globally. And it already has.

Inflation Is Still Too Sticky for Comfort

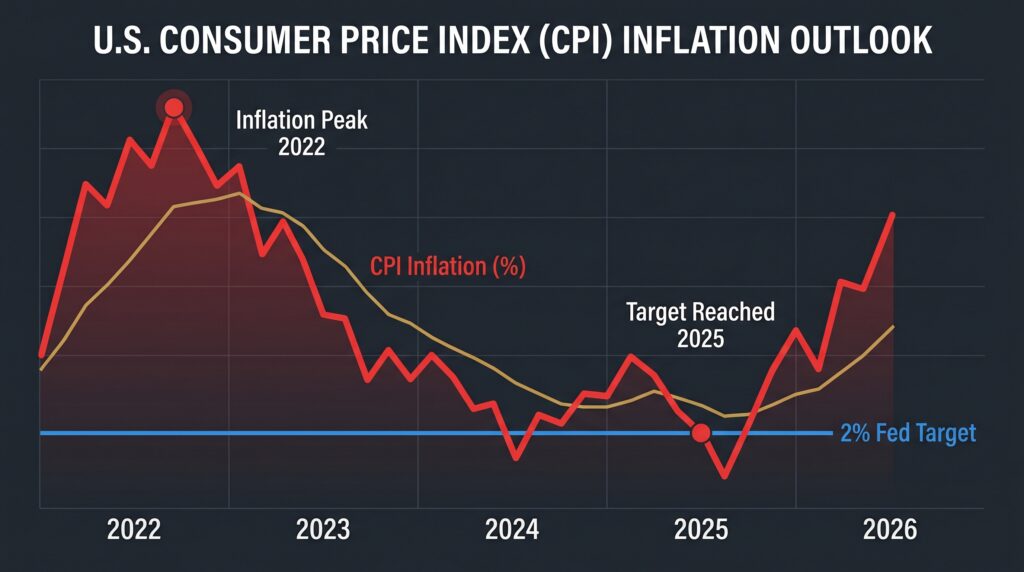

The core problem is that inflation is not falling cleanly back to the Fed’s 2% target — and the most stubborn parts of the price basket are not cooperating.

Headline inflation has moved higher again after a period of gradual cooling through 2024 and early 2025. But the bigger concern for policymakers is what is happening beneath the surface. Some of the most persistent components of the inflation basket — shelter costs and services — continue to show structural rigidity that is not responding to current policy settings. Energy has added a new layer of fresh upward pressure, further complicating the path back to target.

This distinction matters enormously. Central banks do not simply ask whether inflation is lower than last year. They ask whether inflation is firmly and durably under control. Right now, the data does not fully support that confidence — and the Fed knows it.

When inflation remains sticky at levels above target, the central bank cannot afford to sound relaxed, even if it chooses to hold rates steady. That tension between holding rates and managing expectations is the defining challenge of the current monetary policy moment.

The Real Policy Rate: The Story Most Investors Are Missing

One of the most misunderstood dynamics in the current environment is that the Fed’s policy can quietly become less restrictive even when it does nothing at all.

Here is the mechanism that matters:

What counts is not the nominal interest rate. What counts is the real interest rate — the policy rate adjusted for current inflation.

If inflation rises while the Fed holds its nominal target unchanged, then real interest rates fall. In practical terms, monetary policy becomes looser without a single formal rate cut being announced.

This is not a theoretical concern. It is exactly what has been unfolding over the past several months. As US inflation re-accelerated toward 3.8%, the real federal funds rate quietly slipped into negative territory — meaning the Fed’s benchmark rate, adjusted for actual price pressures, is no longer meaningfully restrictive.

For institutional investors and central bank watchers, this is a critical signal. The Fed may feel compelled to initiate a Fed rate hike not because the economy is overheating in an obvious way, but because doing nothing has allowed conditions to passively loosen. That is a subtle but important distinction — and one that keeps the rate hike scenario alive even in a slowing economy.

Why Fed Communication Matters More Than the Rate Decision Itself

Markets do not move only on rate decisions. Increasingly, they move on signals — the carefully chosen language that central bank officials use to prepare the market for what is coming before it officially arrives.

Central bank communication is one of the most powerful policy tools available to the Fed. When influential officials — particularly those with active voting roles on the Federal Open Market Committee — begin warning that inflation remains a genuine risk, they are not speaking casually or speculatively. They are deliberately shifting the market’s probability assessment before a formal policy change is announced.

This is why hawkish language from senior Fed officials deserves serious attention, not dismissal as routine caution.

The implication for investors is direct: the Fed does not need to hike tomorrow to change the investment landscape today. A sustained shift in official rhetoric is often the first and most important signal that the rate environment is transitioning — and portfolios positioned for the old narrative will begin to lag before the policy itself catches up.

The Labor Market Makes This a Genuinely Difficult Call

If price stability were the Fed’s only objective, the case for another hike would be considerably simpler. But the Federal Reserve operates under a dual mandate — it is legally required to pursue both price stability and maximum sustainable employment simultaneously.

And the labor market is no longer providing the cover it once did for aggressive policy action.

Job growth has moderated meaningfully from the elevated pace of the post-pandemic recovery. Unemployment is not alarming, but it is no longer at the historically tight levels that gave the Fed confidence to hike aggressively in 2022 and 2023. Wage growth remains solid but is not running at a pace that suggests the labor market is generating its own independent inflationary impulse.

This creates the defining policy dilemma of the current cycle:

- Hike too aggressively and risk pushing a moderating labor market into a sharper-than-intended contraction.

- Wait too long and risk allowing inflation to become more deeply embedded in expectations, wages, and pricing behavior — requiring an even harder landing later.

The Fed is not choosing between a right answer and a wrong one. It is navigating between two imperfect paths, with incomplete data on both sides. That uncertainty is precisely what makes the current environment so difficult to price — and so important to monitor actively.s the current environment so difficult to price — and so important to monitor actively.ult to price — and so important to monitor actively.

The Real Risk: When Inflation Gets Into People’s Heads

This is the dimension of the current debate that deserves the most serious attention from long-term investors.

Inflation becomes structurally dangerous not simply because prices are high today, but because of what happens when people start expecting prices to stay high tomorrow. Once that psychological shift takes hold, businesses begin pricing more aggressively in anticipation of rising costs. Workers negotiate higher nominal wages to protect their real purchasing power. Consumers accelerate purchases to beat future price increases. Each of these behaviors independently reinforces the inflation that triggered them.

That is how inflation transitions from a short-term commodity or supply-side disruption into a structural, self-sustaining economic condition — far harder and more painful to reverse.

And once inflation expectations become unanchored, the eventual policy response required to restore credibility is typically more severe, not more gradual. The historical record on this point is unambiguous. Central banks that moved early contained the problem with less economic damage. Those that moved late paid a significantly higher price in growth, employment, and financial stability.

Even if the Fed ultimately does not hike, the risk that long-term expectations drift higher is itself enough to keep policymakers on an elevated state of alert — and enough to keep investors cautious about assuming that the next policy move is a benign cut.

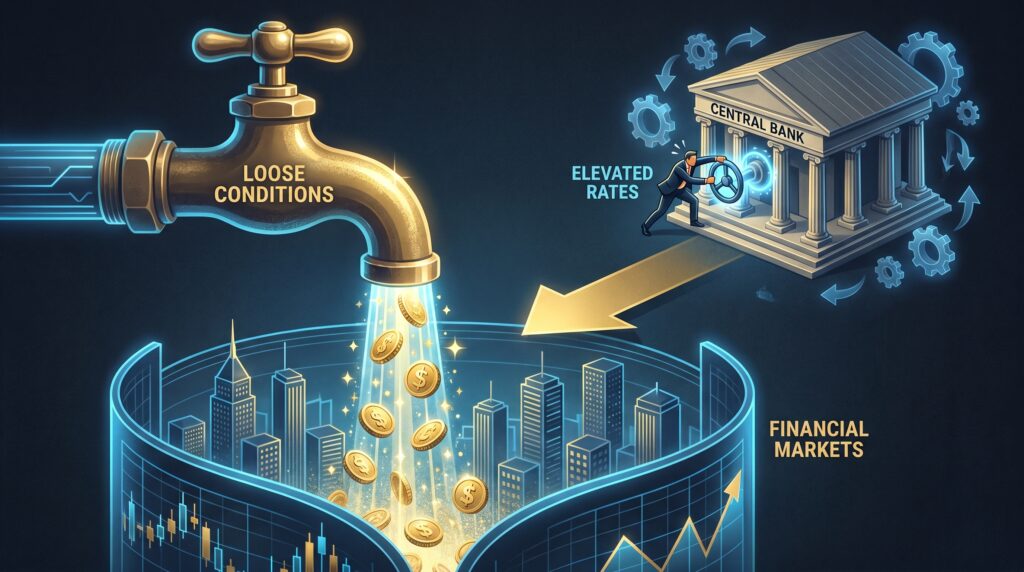

Financial Conditions May Still Be Too Loose

Here is another reason the market may be underestimating the probability of further Fed tightening — and it is perhaps the most counterintuitive element of the current cycle.

Even with policy rates sitting at multi-year highs, broader financial conditions have not become meaningfully restrictive in practice. Corporate credit markets remain liquid. Capital access for institutional borrowers remains broadly available. Asset prices have shown resilience well beyond what traditional monetary transmission models would predict at this rate level.

Objective measures confirm this. The Chicago Fed National Financial Conditions Index — a broad composite indicator that tracks the tightness or looseness of US financial conditions — is currently printing in deeply negative territory, well below its historical average. In plain terms: the financial system is operating in looser-than-average conditions despite nominal rates sitting above 3.5%.

This matters because the Federal Reserve does not look exclusively at its own policy rate in isolation. It also evaluates how that rate is actually transmitting into the real economy and the broader financial system. If credit remains easy, markets remain liquid, and corporate investment continues despite elevated nominal rates, the central bank may rationally conclude that current settings are simply not tight enough to achieve the disinflation it needs.

That conclusion — that policy is insufficiently restrictive — is precisely the analytical foundation from which a rate hike becomes not just possible, but logically necessary.

What a More Hawkish Fed Means for Global Investors

If the Federal Reserve turns materially more hawkish through the second half of 2026, the consequences will not remain contained within US borders. Because the US dollar functions as the foundational reserve and trade settlement currency of the global financial system, any shift in Fed posture generates immediate and measurable transmission effects across every major market.

1. The US Dollar Could Strengthen

Higher US interest rates make dollar-denominated assets more attractive to global capital. Institutional investors holding foreign-currency assets face increasing incentive to rotate into higher-yielding US instruments, mechanically bidding up the greenback in the process.

A sustained period of dollar strength creates downstream stress for countries that rely heavily on USD-denominated imports or carry significant dollar-denominated debt on their sovereign or corporate balance sheets.

2. Emerging Markets Could Face Renewed Pressure

Emerging market economies are historically among the most exposed to Fed tightening cycles. When US yields rise and the dollar strengthens simultaneously, foreign capital becomes more selective about EM exposure. Currencies can weaken sharply. Imported inflation can worsen. The cost of servicing external dollar debt escalates in local-currency terms.

For investors with exposure to Indian, Southeast Asian, Latin American, or African equity and fixed income markets, this dynamic deserves direct attention. FPI flows, currency volatility, and domestic monetary policy responses in EM economies are all meaningfully affected by the Fed’s stance.

3. Equity Valuations Face Structural Headwinds

Higher risk-free rates reduce the present value of future cash flows — which is the mathematical foundation of equity valuation. This effect is most severe for long-duration growth stocks, where the bulk of projected earnings are discounted from many years into the future.

Sectors historically under pressure during unexpected tightening cycles:

- High-multiple technology and speculative growth

- Leveraged real estate and rate-sensitive utilities

- Non-earning enterprises valued purely on future potential

Sectors that have historically demonstrated relative resilience:

Defensive consumer staples with consistent free cash flowvalue stocks, defensive sectors, and some commodity-linked names may hold up better.

Cash-generating businesses with genuine pricing power

Value-oriented and short-duration equities

Commodity producers with direct inflation exposure

4. Bonds May Not Feel As Safe As Expected

Many investors entered 2026 with portfolios positioned for the rate-cut scenario — holding longer-duration bonds in anticipation of capital appreciation as yields fell. If the market begins systematically pricing in renewed hiking risk, those positions face meaningful mark-to-market losses.

Duration risk — the sensitivity of a bond’s price to changes in yield — matters more than many retail and institutional investors currently appreciate in this environment. The old playbook of buying long bonds ahead of expected Fed cuts may need to be revisited entirely.

Five Indicators That Will Decide Whether This Hike Becomes Real

Rhetoric and risk scenarios only become actionable when they are anchored to specific, trackable data points. These are the five indicators that will most directly determine whether a 2026 Fed rate hike moves from possibility to probability:

Indicator 1: Inflation Data (CPI and PCE)

This remains the master variable. If headline and core inflation remain elevated — particularly in services and shelter — the Fed will struggle to justify any dovish pivot. Monthly CPI and PCE releases are the single most market-sensitive data points in the current cycle.

Indicator 2: Wage Growth

Sustained nominal wage growth running well above the level consistent with 2% inflation is the clearest signal that price pressures are becoming embedded in the labor market. Watch the BLS Average Hourly Earnings release and the quarterly Employment Cost Index for early warning.

Indicator 3: Employment Reports

A resilient labor market provides the Fed with the political and economic flexibility to prioritize inflation control. A sharp deterioration in nonfarm payrolls or a spike in unemployment would dramatically complicate the case for further tightening — even if inflation remains above target.

Indicator 4: Fed Language and Official Communications

There is a material difference between “monitoring inflationary risks” and “prepared to act if conditions warrant.” Watch for any language shift in FOMC statements, Fed Chair press conferences, and regional president speeches. Hawkish language upgrades from multiple voting members in the same window are the clearest pre-announcement signal available.

Indicator 5: Financial Conditions Indices

If broad financial conditions — measured by credit spreads, capital market liquidity, and asset price behavior — remain loose despite elevated nominal rates, the Fed may conclude that its current settings are achieving less real-economy cooling than intended. That conclusion directly supports the case for additional tightening.

The Bottom Line

Markets entered 2026 with a clear and comfortable consensus: inflation was beaten, cuts were coming, and the investment landscape would become progressively more accommodative.

That consensus is under serious pressure.

Inflation is still running above target. The real policy rate has quietly slipped into negative territory. Financial conditions remain looser than the headline rate suggests. And senior Fed officials are openly raising the possibility that current settings may not be tight enough to finish the job.

None of this guarantees another rate hike. But it does mean that investors who are still positioned exclusively for the old narrative — the one built on the assumption that cuts were the only direction left — are carrying more risk than they may realize.

The biggest mistake in the current environment is not getting a call wrong. It is refusing to update when the data changes.

Global markets will not wait for a formal announcement before repricing. They are already beginning to move. The question is not whether investors should pay attention to this shift — it is whether they are paying attention early enough to matter.

FAQ

Is the Fed likely to hike rates again in 2026?

It is not guaranteed, but the possibility is clearly back on the table. Sticky inflation and persistently loose financial conditions are the two conditions most likely to push the Fed toward action. Neither has fully resolved.

Why does a Fed rate hike matter for global investors?

Because US interest rates directly influence the dollar, global capital flows, sovereign and corporate bond yields, emerging market financial conditions, and equity valuations worldwide. A Fed hike is a global event, not a domestic one.

Which asset classes tend to underperform when US rates rise unexpectedly?

Long-duration government bonds, high-multiple growth equities, leveraged real estate, and rate-sensitive utility stocks have historically shown the greatest vulnerability during unexpected Fed tightening cycles.

Can the Fed stay on hold and avoid hiking entirely?

Yes — a prolonged pause remains possible if inflation cools and labor market conditions deteriorate meaningfully. The key message for investors is not that a hike is certain, but that rate cuts are no longer the only scenario worth preparing for.

What should investors do to prepare?

This article is for educational purposes only and does not constitute investment advice. Investors should consult a qualified financial professional before making portfolio decisions based on macro scenarios.

Also read:

- What Happens to Your SIP When Market Falls 40%?

- US-Iran Peace Deal: Inflation Impact on Rate Cuts in 2026

- Market Volatility: 3 Reasons Indian Investors Shouldn’t Panic

- SIP vs Lumpsum: Which is Better for You?

Final Disclaimer

This article is for educational and informational purposes only. It does not constitute financial, investment, legal, or tax advice. Market conditions and central bank policy expectations can change rapidly. All data cited is derived from publicly available sources including the Bureau of Labor Statistics, Bureau of Economic Analysis, Federal Reserve, CME Group, and Chicago Federal Reserve. Please conduct your own research and consult a qualified financial professional before making any investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.