FII Outflows India 2026: What Record Foreign Selling Means for Your Portfolio, EMIs, and Savings

The headlines look terrifying. “FII Bloodbath.” “Rupee at All-Time Low.” “₹1.17 Lakh Crore Dumped in a Single Month.”

But before you make any decisions about your portfolio — stop, breathe, and read this.

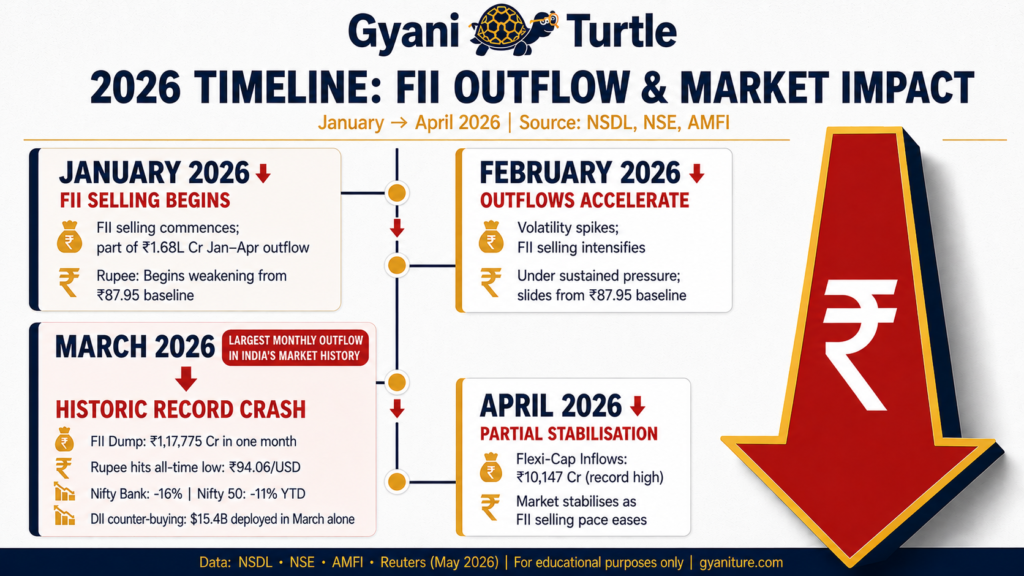

FII outflows India 2026 have hit historic levels. Between January and April 2026, Foreign Portfolio Investors pulled over $20 billion (₹1.68 lakh crore) out of Indian equities — already surpassing the entire outflow recorded in calendar year 2025. March 2026 alone saw ₹1,17,775 crore (~$11 billion) exit in a single month — the largest monthly net outflow in Indian market history.

Your mutual fund portfolio is in the red. Your home loan EMI just jumped. And every financial news channel is competing to explain why India’s market is correcting.

What is happening right now is not new. It is not the end of India’s growth story. The investors who understand the mechanism behind this sell-off will emerge from it significantly wealthier than those who panic.

This is your complete, data-backed breakdown of the FII outflows India 2026 crisis: what triggered it, how it reaches your dinner table, and exactly what a patient investor does right now.

📌 Regulatory Disclaimer: This article is for educational and informational purposes only and does not constitute financial or investment advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future results. Consider consulting a SEBI-registered investment advisor (RIA) for personalised financial planning.

The Scale of FII Outflows India 2026: Historic Numbers

Let us start with the numbers, because they are genuinely historic.

Between January and April 2026 alone, Foreign Portfolio Investors (FPIs) pulled over $20 billion (approximately ₹1.68 lakh crore) out of Indian equities. To put that in perspective: this single four-month figure already surpasses the $18.9 billion total outflow recorded across the entirety of calendar year 2025.

March 2026 was the epicentre. FIIs offloaded a staggering ₹1,17,775 crore (~$11 billion) in that single month — the largest monthly net outflow in Indian market history, surpassing the previous record of $10.9 billion set in October 2024. The full monthly FPI transaction data is publicly available on the NSDL official FPI tracking portal

Understanding what is driving FII outflows India 2026 requires

looking at two simultaneous macro forces that converged in early 2026.

The collateral damage across Indian markets has been significant:

- The Nifty 50 fell 8.2% to 11% year-to-date by early May 2026

- The Sensex dropped 9.8% to 12% YTD

- The Nifty Bank index collapsed 16% during the March liquidation — its worst single-month performance in 6 years

- FII ownership within the Nifty 50 cratered to approximately 24.1% — a 13 to 15 year historical low

The Indian Rupee paid the heaviest price: it touched an intraday all-time low of ₹94.06 per USD in late March 2026, a sharp fall from the ₹87.95 levels seen earlier in 2025.

This is the data. Now let us understand why it happened — because the “why” determines everything about how you should respond.

Why FII Outflows India 2026 Hit Record Levels

This is not a story about India failing. It is a story about global capital following the path of least resistance.

Two simultaneous macro forces converged in early 2026 to make this mathematically inevitable for global fund managers:

Force 1 — The US Bond Magnet: US 10-year Treasury yields surged past 4.4% — a sharp 50-basis-point jump in a matter of weeks. When risk-free US government bonds offer 4.4% in hard dollars, global mega-funds mathematically recalibrate. The risk premium required to justify holding volatile emerging market equities suddenly demands justification. For many funds, India’s valuations — stretched after the 2023-2024 bull run — no longer offered sufficient cushion. Current US Treasury yield data is tracked live on the US Federal Reserve H.15 release page.

Force 2 — The Crude Oil Shock: West Asian geopolitical escalations pushed Brent crude above $100 per barrel. For India, which imports approximately 90% of its crude oil needs, this is not just a global commodity story — it directly threatens India’s current account deficit, currency stability, and corporate profit margins simultaneously.

As one Kotak Market Insights note summarised the dynamic: with Brent oil over $100 threatening India’s current account and risk-free US yields at 4.4%, global mega-funds are structurally compelled to pull capital from highly-valued emerging markets and park it back in safe-haven dollar assets.

The sectors that bore the worst of the selling reflect this logic precisely. The Banking and Financial Services sector — India’s most liquid and FII-owned space — saw over ₹79,981 crore ($8.44 billion) liquidated. IT services, the second most FII-concentrated sector, lost approximately ₹22,000 crore in foreign holdings.

This was not random panic. It was systematic, rational portfolio rebalancing by global capital — which makes it both understandable and survivable.

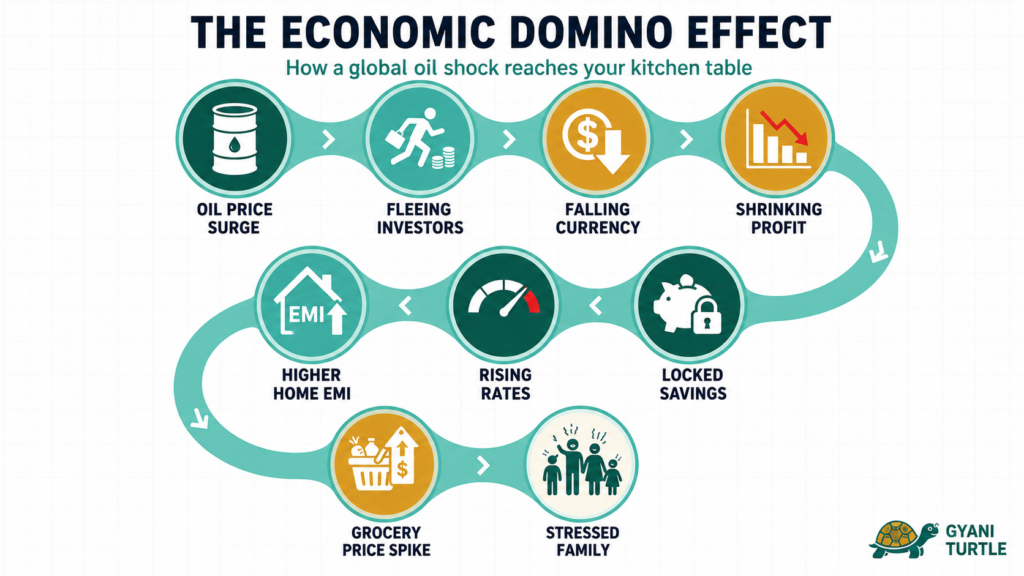

How a Global Sell-Off Reaches Your Kitchen Table

This is the chain reaction that never gets explained clearly in mainstream financial media.

Step 1 — The Global Trigger: Geopolitical conflict in West Asia chokes energy corridors, spiking Brent crude past $100/barrel. Simultaneously, the US Fed maintains high rates, pushing Treasury yields to 4.4%.

Step 2 — The FII Flight: Foreign investors realise they can earn risk-free returns in US dollars. They mass-sell high-valuation Indian blue-chip stocks — HDFC Bank, Reliance, Infosys — to lock in multi-year profits.

Step 3 — The Currency Hit: To repatriate their money, FIIs convert Indian Rupees to US Dollars. This massive INR dumping crashes the Rupee to its all-time low of ₹94.06 per dollar. A key consequence of FII outflows India 2026 is the currency hit — as FIIs convert Rupees to Dollars to repatriate capital, the Rupee crashes to its all-time low of ₹94.06 per USD.

Step 4 — The Imported Inflation Wave: Because India imports nearly 90% of its crude oil, every barrel now costs dramatically more in rupee terms. Oil marketing companies absorb this — briefly — before passing it downstream.

Step 5 — The Transportation Spike: Diesel prices rise. The cost of trucking vegetables, milk, and daily essentials from farms to urban distribution hubs spikes across the country.

Step 6 — The Corporate Squeeze: Manufacturing and consumer goods companies face a double squeeze — rising raw material import costs and higher domestic logistics costs. Profit margins compress. Corporate earnings guidance is cut. This triggers further stock market corrections.

Step 7 — The RBI’s Defensive Bind: To prevent the Rupee from collapsing further and to tame rising import-led inflation, the RBI is forced to keep repo rates elevated rather than cutting them to stimulate growth.

Step 8 — The EMI Hammer: Commercial banks transmit these elevated rates to consumers. Floating home loan, car loan, and personal loan EMIs rise.

Step 9 — The Retail Backlash: The ordinary Indian family now faces higher grocery bills, higher fuel costs, and higher loan EMIs — simultaneously. Disposable income shrinks. Discretionary spending drops. Corporate revenue growth slows. The cycle feeds itself.

This is why a geopolitical event in West Asia ends up affecting whether a family in Pune can afford their child’s coding class this month.

One Story. Two Outcomes.

Meet the Sinhas — Rajesh (42, IT Project Manager) and Anjali (39, Private School Teacher), living in Pune.

Their financial profile:

- Combined monthly net income: ₹1,85,000

- Active home loan: ₹55 Lakhs at a floating interest rate

- Mutual fund portfolio: ₹18 Lakhs, built via ₹35,000/month SIPs

When the headlines screamed “₹1.17 Lakh Crore FII Bloodbath” and the Rupee crossed ₹94, their portfolio dropped from ₹18 Lakhs to ₹15.8 Lakhs on paper. Simultaneously, their bank sent a notification: floating rate adjustment — monthly EMI increasing by ₹6,200.

The Sinha family of Pune is a perfect illustration of how FII outflows India 2026 affect ordinary household finances — and how two different responses lead to completely different financial outcomes.

Two paths opened up.

❌ The Wrong Path: Panic Liquidation (Rajesh’s Instinct)

Terrified by the news cycle, Rajesh logs in and stops all active SIPs. He then goes further — he liquidates the entire equity mutual fund portfolio, locking in a real capital loss of ₹2,00,000. The remaining ₹15.8 Lakhs moves into a standard savings account earning 3% — a return well below inflation.

To handle the ₹6,200 EMI increase, the family cuts their health insurance top-up and cancels their children’s educational subscriptions.

The long-term damage: When the market recovers 14 months later, the Sinhas are holding depreciating cash that has lost real purchasing power. They bought zero units during the period when Indian equities were cheapest. Their financial goals are set back by years — not because the market failed them, but because they exited at the worst possible moment.

✅ The Right Path: Strategic Rebalancing (Anjali’s Plan)

Anjali steps back from the noise and looks at the historical context. She recognises that this FII selling is a cyclical liquidity and valuation event — not a structural collapse of the Indian economy.

The family executes a calm, three-step response:

1. They keep all ₹35,000/month SIPs running without interruption. They slightly rebalance — trimming some volatile mid-cap allocation and redirecting it into heavily discounted, resilient large-cap blue-chip funds.

2. They pause a planned international vacation, freeing up ₹1,50,000 in discretionary cash.

3. They deploy ₹1,00,000 of that saved cash as a direct principal prepayment on their home loan — reducing the outstanding principal and neutralising most of the EMI increase without needing to touch their investments.

The long-term reward: Their paper loss remains a paper loss and never becomes real. Their ₹35,000 monthly SIP during the downturn accumulates nearly double the unit count at discounted NAVs. When FIIs inevitably return to Indian equities and the market recovers, their expanded unit base amplifies the upswing disproportionately. Their retirement timeline accelerates by approximately 3 years compared to the pre-crisis projection.

The only difference between these two outcomes was a decision made in one week of maximum fear.

Where to Invest During the FII Outflows India 2026 Crisis

|

Asset Choice |

Personal Return Profile |

Risk Level |

Tax Angle (2026) |

Supports India? |

|---|---|---|---|---|

|

Large-Cap Equity Funds / Index ETFs |

12–15% long-term CAGR post-recovery consolidation |

Moderate to High (short-term volatile; low structural risk) |

12.5% LTCG on gains above ₹1.25 Lakh per year |

Yes — directly absorbs FII selling pressure and provides liquidity to top Indian companies |

|

Sovereign Gold Bonds (SGB) / Digital Gold |

8–10% (dependent on global risk-off spikes) |

Low (sovereign backing; price tied to international gold) |

SGB capital gains fully tax-exempt if held to maturity |

Neutral — does not fund Indian corporate capital expenditure |

|

Short-Term Corporate Debt / T-Bills |

7.5–8.5% (elevated yield due to high RBI repo rates) |

Very Low (high-quality AA+ corporate or government paper) |

Taxed at your income slab rate |

Yes — funds working capital of Indian firms during liquidity stress |

|

Panic Cash (Savings / Physical) |

3–3.5% (guaranteed real-value destruction via inflation) |

Extreme risk to purchasing power |

Interest above ₹10,000 taxed at slab rate |

No — starves the domestic financial system of productive capital |

The table above maps what your money does — and does not do — in each scenario. The critical insight: during an FII outflow, the most patriotic and the most personally profitable choice are the same thing. Domestic retail capital stepping in to buy what foreign funds are selling is both a civic and a financial act.

And the data confirms this is exactly what happened. Domestic Institutional Investors (DIIs), powered by retail SIPs, deployed a record $15.4 billion (approximately ₹1.29 lakh crore) in March 2026 alone — directly absorbing the historic FII dump and preventing a full-blown systemic market crash.

Indian retail investors, collectively, saved the market.

What You Must Do Right Now

For Salaried Professionals

Do not stop the SIP engine. Your regular salary is your greatest structural advantage. Your automated monthly investment is currently buying the best companies in India at a 10–15% discount from their recent highs. Every instalment you skip is a discounted unit you will never recover.

On the debt side: if you have surplus variable pay, performance bonuses, or festival increments, direct them as lump-sum principal prepayments on your floating-rate home loan. This tactically reduces your outstanding balance and offsets future EMI increases without requiring you to touch your investments.

For Business Owners and MSME Operators

Conserve working capital aggressively. With the Rupee weak and credit conditions tight, delay heavy capital expenditure plans that require imported components or foreign machinery until currency volatility stabilises below ₹90.

If your business relies heavily on raw material imports, explore forward contracts with your bank or financial advisor to lock in exchange rates and protect your operating margins from further Rupee depreciation.

For Active Investors

Execute tactical rebalancing — not panic selling. Review your portfolio’s risk distribution. If you are overexposed to high-beta, unproven small-caps, trim those positions selectively and rotate the capital into high-quality, cash-rich large-cap financial and capital goods stocks that have been beaten down primarily due to FII volume selling rather than deteriorating fundamentals.

If you have cash on the sidelines, deploy it in tranches rather than trying to time the absolute bottom. A staggered approach — deploying 20% every month over five months into diversified index funds — removes the emotional burden of market timing while ensuring you participate in the recovery.

For Families and Homemakers

Audit discretionary spending immediately. With imported inflation driving up transportation, fuel, and grocery costs, a strict 3-month pause on high-ticket lifestyle upgrades and luxury subscriptions frees up real cash for more productive uses.

Build what we call an EMI Protection Pool: liquidate idle money sitting in low-yield savings accounts and lock it into short-term Fixed Deposits or recurring deposits at current elevated rates. Keep this pool explicitly earmarked to cover any sudden floating-rate EMI increases — so your investment portfolio never becomes the emergency fund.

The Critical View: What the Optimistic Narrative Misses

The mainstream financial media is celebrating Indian retail investors as heroes for absorbing FII selling. That is true — but it deserves a harder, more honest examination.

The Retail Cushion Trap. Critics raise a legitimate concern: domestic retail money is effectively being used as an exit cushion for sophisticated global funds. FIIs are locking in massive multi-year profits from Indian equities accumulated at 2020-2021 valuations — and exiting at premium 2024-2026 prices. Ordinary Indian retail investors, who entered at higher valuations via ongoing SIPs, are now holding the paper losses while global capital books the gains.

The Valuation Reality. Skeptics point out that India’s domestic market cannot decouple from global economic fundamentals indefinitely. If corporate earnings growth continues to slow — due to high input costs, rural consumption stress, and compressed margins — domestic SIP inflows will eventually moderate. When that happens, the absence of FII support could expose markets to a deeper structural correction than the current cyclical sell-off.

The Middle-Class Squeeze. The government’s celebration of market stability sits uncomfortably alongside ground realities. The Indian middle class is being hit from both sides — facing paper losses in investment portfolios while simultaneously absorbing higher food inflation and rising loan EMIs driven by the RBI’s defensive interest rate posture. The macro narrative of “resilience” is not evenly distributed.

These are not reasons to panic or exit. They are reasons to invest with clear eyes — understanding the structural complexity beneath the surface.

What India’s Institutions Are Doing

The Reserve Bank of India (RBI) has deployed a proactive defence. The central bank is actively intervening in both the spot and forward foreign exchange markets — selling dollars from India’s forex reserves to smooth out Rupee depreciation and prevent speculative cascades past the ₹94–95 zone. As RBI Governor Shaktikanta Das stated in April 2026: India’s domestic capital pools are no longer just passive shock absorbers — they are the core foundational pillars of market liquidity.

SEBI has intensified regulatory monitoring of systemic risk, particularly within equity derivative (F&O) segments. The regulator is pushing for enhanced capital adequacy disclosures from brokers and fast-tracking frameworks to deepen domestic institutional participation — reducing India’s structural dependence on FII flows for market stability.

The Ministry of Finance maintains that the current sell-off is a temporary valuation-alignment event. Government economic advisors argue that India’s projected real GDP growth of 6.5% to 7% makes it an unavoidable long-term destination for global capital — and that flows will return as global risk aversion normalises.

The RBI publishes weekly forex reserve and intervention data on the RBI Weekly Statistical Supplement.

The Gyani Turtle Verdict on FII Outflows India 2026

FII outflows India 2026 are not without precedent. They are not unique to India. And they are not permanent.

In 2008, FIIs sold. In 2013’s taper tantrum, FIIs sold. In 2018’s rate cycle, FIIs sold. In 2020’s pandemic shock, FIIs sold. Every single time, the patient domestic investor who held the line — or better, who kept buying — was rewarded substantially when the cycle turned.

The 2026 outflow is different in scale. It is not different in nature.

Here is the patient investor’s framework for navigating an FII crisis:

Understand the mechanism. This is a valuation and yield trade, not a verdict on India’s long-term growth. Global capital will return when US yields normalise and crude oil retreats. The question is whether your units will be waiting for it.

Let your SIP be the hero. Your ₹10,000 monthly instalment is buying more units today than it bought a year ago. That is not a problem. That is the entire point of systematic investing.

Protect your debt first. Use surplus cash to reduce your floating-rate loan principal rather than making impulsive investment decisions driven by fear or greed.

Rebalance toward quality, not away from equity. Trim unproven small-caps if needed. Move toward large-cap, cash-rich fundamentally strong businesses that have been dragged down by FII volume selling alone — not by deteriorating business performance.

Turn off the news cycle. Daily headlines about FII selling are designed to generate anxiety, not to help you invest better. The data — historical recovery timelines, SIP continuity returns, domestic DII absorption — tells a calmer, clearer story.

India’s market bottomed and recovered after every major FII outflow in its history. The investors who kept their SIPs running through each of those cycles built the most wealth. The ones who stopped are still calculating what they lost.

Invest like a patient investor.

|

Metric |

Verified Value |

Source |

|---|---|---|

|

YTD 2026 FPI equity outflow (Jan–Apr) |

Over $20 billion (~₹1.68 lakh crore) |

Reuters / NSDL, May 2026 |

|

March 2026 single-month FII outflow |

₹1,17,775 crore (~$11 billion) |

NSDL Official Ledger, March 2026 |

|

Full FY 2024–25 FPI net sales |

₹1,27,041 crore |

NSDL / The Hindu, April 2025 |

|

Intraday Rupee all-time low |

₹94.06 per USD |

Forex Spot Records, March 2026 |

|

US 10-year Treasury yield peak |

~4.34%–4.4% |

US Federal Reserve Data, March 2026 |

|

Brent crude price benchmark |

Above $100/barrel |

ICE Brent Futures, May 2026 |

|

FPI liquidations from financials |

₹79,981 crore ($8.44 billion) |

Sectoral FPI Disclosures, May 2026 |

|

FII ownership in Nifty 50 |

~24.1% (13–15 year low) |

NSE Shareholding / Finology, May 2026 |

|

Nifty Bank single-month correction |

-16% |

NSE Performance Logs, March 2026 |

|

DII inflows in March 2026 |

$15.4 billion (~₹1.29 lakh crore) |

AMFI / Kotak Securities, May 2026 |

📌 All data is sourced from NSDL, NSE, BSE, AMFI, Reuters, RBI briefings, and public AMC research notes. All return projections are indicative historical averages and do not guarantee future performance. Please verify current figures directly on NSDL.co.in, AMFI.in, or your fund house’s website before making investment decisions.

Also read:

- Silicon Nationalism: Why Apple Just Hired Its Most Famous Ex to Build Its Chips

- How to Use Agentic AI in Investment and Trading — A Complete Guide for Indian Investors

- Start Investing in India — Best Essential Beginner’s Guide 2026

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before making investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.

One Comment