Silicon Nationalism: Why Apple Just Hired Its Most Famous Ex to Build Its Chips

In 2020, Apple did something that shocked the technology world. Apple Intel deal

It publicly fired Intel.

After a decade of frustration with Intel’s manufacturing delays and power-hungry processors, Apple announced its own M-series chips — designed in-house, manufactured by Taiwan’s TSMC, and delivering performance that made Intel’s best work look embarrassingly dated. The divorce was clean, total, and seemingly permanent. Intel was out. Apple Silicon was in.

Fast-forward to May 2026.

Apple is now reportedly in serious advanced talks to hire Intel — not to design chips, but to manufacture them. The world’s most valuable company wants the world’s most troubled chipmaker to build its processors in American factories.

This is not a reconciliation. This is a geopolitical manoeuvre dressed in a business suit.

And if you’re a global investor, it is one of the most important stories of 2026.

First — What Is the Apple Intel Deal Actually About?

Let’s be precise, because most headlines are getting this wrong.

Apple is NOT putting Intel chips back in its computers.

The M-series chips — the brilliantly designed processors that power your MacBook Air and iPad — are still Apple’s own designs. Apple is not going back to buying processors from Intel. What Apple is doing is far more interesting.

Apple wants Intel to manufacture Apple’s own chip designs using Intel’s new 18A fabrication process.

Think of it like this: Apple is the architect who designed a brilliant building. For years, they hired one builder — TSMC in Taiwan — to construct every building. Now they want to hire a second builder — Intel in America — to construct some of those buildings too. The design stays Apple’s. The blueprint stays Apple’s. But the construction is distributed.

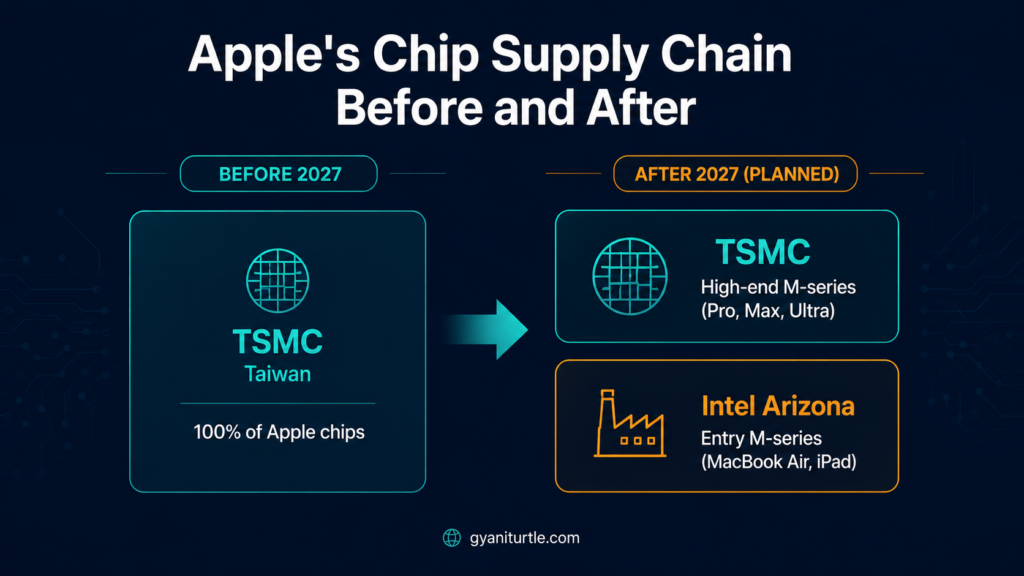

The potential collaboration would see Intel handling production of Apple’s lowest-end M-series chips using its advanced 18A-P manufacturing process, while TSMC continues manufacturing the higher-performance variants.

Specifically — the chips that power the MacBook Air and entry-level iPad Pro. Apple plans to use the Intel 18A-P process for its lowest-end M-series processors, with shipments expected to begin around the second quarter of 2027, with initial annual volumes between 15 million and 20 million chips.

Your iPhone? Still TSMC. The M5 Pro in the MacBook Pro? Still TSMC. This is a surgical, carefully designed entry — not a wholesale shift.

The TSMC Problem Nobody Was Talking About

To understand why Apple is doing this, you need to understand the single largest supply chain risk in modern consumer technology.

Apple has been 100% dependent on one company — TSMC — for every advanced chip in every product it sells. iPhones, iPads, MacBooks, Apple Watches, AirPods chips — all manufactured in Taiwan by a single supplier.

Taiwan sits 180 kilometres from mainland China.

The company remains anchored to TSMC for its most advanced products, from iPhones to the higher-end M-series parts, but has been pursuing greater supply chain redundancy since the 2020-2022 disruption cycles.

The AI boom made this worse. Apple gains immense bargaining power and a critical safety net by bringing Intel into the fold. This strategy allows Apple to bifurcate its lineup: keeping its highest-end “Pro” and “Max” chips with TSMC in Taiwan and Arizona, while shifting its massive volume of entry-level MacBook Air and iPad silicon to Intel’s domestic fabs.

For a company sitting on $180+ billion in cash and whose entire revenue engine depends on uninterrupted chip supply — distributing that dependency is not optional. It’s existential risk management.

The Technology: Why Intel 18A Actually Matters

Here is the part that separates this story from hype.

For years, “Intel is catching up to TSMC” was a recurring headline that never quite materialised. 10nm was late. 7nm was cancelled. The company that invented modern chip manufacturing kept embarrassing itself while TSMC pulled further ahead.

18A is different. The numbers back it up.

Intel’s 18A yields have improved to over 60%, good enough to ramp Panther Lake. While not best in class — TSMC was at 70–80% when it launched 2nm — with Intel’s aspirations of being the second foundry supplier, 60%+ yield is significantly better than SF2 at Samsung Foundry, which is believed to be less than 40%.

What makes 18A technically significant is two innovations that Intel brought to market first:

RibbonFET — a new transistor architecture that allows more transistors in the same space, improving performance and efficiency simultaneously.

PowerVia — backside power delivery, meaning the power supply network is moved to the back of the chip wafer rather than the front. This frees up more space for data pathways and dramatically improves power efficiency.

Intel’s 18A currently holds a performance edge. This is largely attributed to Intel being the first to market with backside power, a feature TSMC is not expected to implement until its N2P or A16 nodes later in 2026 or 2027.

In plain terms: for the first time in nearly a decade, Intel is shipping a manufacturing process that is genuinely competitive with TSMC — and in at least one key dimension, technically ahead.

The Geopolitical Layer: America’s Most Strategic Investment

Now for the part that makes this story genuinely unique in the history of the semiconductor industry.

The U.S. government took a 9.9% equity stake in Intel in the fall of 2025. Washington is now Intel’s largest single shareholder. The world’s most powerful government has made a bet — with taxpayer money — that Intel becomes America’s domestic chip champion.

The strategic logic is not subtle. If Apple, the world’s most valuable consumer brand, manufactures its chips in American Intel factories — that is the single most powerful proof-of-concept that American semiconductor manufacturing is viable and competitive at the frontier.

The move would align with Washington’s push for more domestic semiconductor manufacturing. Intel’s Arizona fabs are central to that policy and would be natural candidates to host 18A for an Apple order.

Under CEO Lip-Bu Tan, who took over in early 2025, Intel has transformed its culture, cut headcount, sharpened execution, and delivered on commitments that the previous leadership consistently missed. Intel’s data center revenue grew 22% in Q1 2026 compared to the same period last year.

Intel has also attracted a roster of foundry customers that would have been unthinkable two years ago — Google (Alphabet) has expanded its AI infrastructure partnership with Intel, and SpaceX is reportedly exploring Intel Foundry for future chip production. An “Apple-certified” 18A process would likely trigger a stampede of other fabless chip designers toward Intel.

This is why the Apple deal matters beyond Apple. It is a credibility stamp that unlocks everything else.

The Investment Reality: Intel’s Stock vs Intel’s Business

Here is where the Gyani Turtle instinct kicks in — and where we need to separate the story from the stock price.

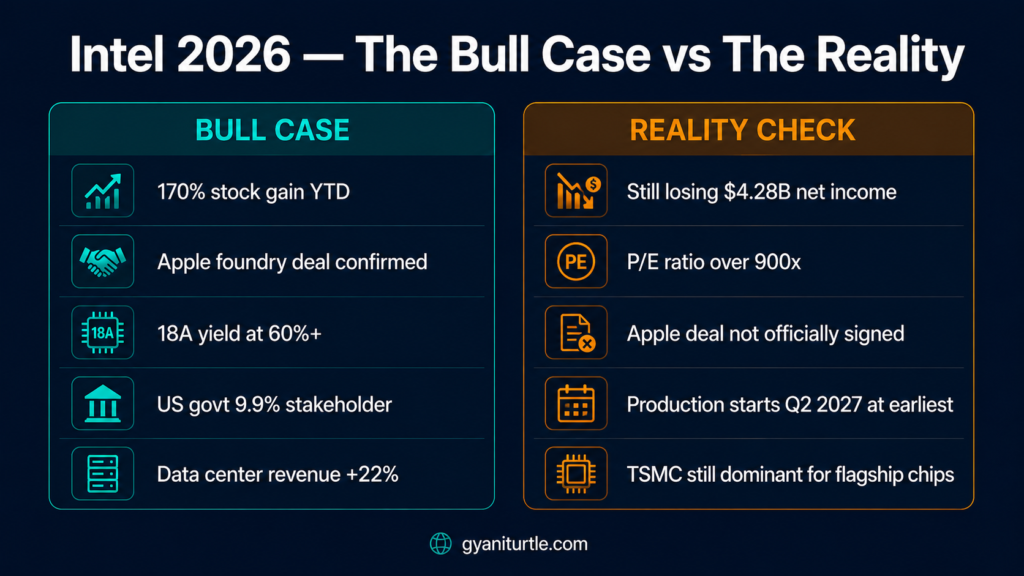

Intel’s stock has surged dramatically in response, rising about 170% in 2026 already. The INTC price reached its all-time high of $114.41 on May 7, 2026.

That is an extraordinary move. And it deserves extraordinary scrutiny.

Here is what the headlines are not telling you:

Intel is still losing money. In its latest quarterly earnings, Intel reported a net income loss of $4.28 billion. Intel’s stock is extraordinarily expensive right now, with a trailing P/E ratio of over 900. It’s hard to justify buying Intel at this highly inflated price.

Read that again. A P/E ratio of over 900. For context, a “fairly valued” mature tech company typically trades at 20–35x earnings. A high-growth tech darling might justify 50–80x. 900x means the market has priced in years — perhaps decades — of flawless execution, zero competition, and continuous margin expansion. That is not an investment. That is a bet.

The Apple deal is also not finalised. It is confirmed by credible analysts and backed by technical due diligence — but it is not a signed, announced, production-scale contract. Production doesn’t even begin until Q2 2027 at the earliest. A lot can go wrong between a preliminary foundry agreement and 20 million chips shipping out of an Arizona factory.

What This Means for Different Investors

Holding AAPL:

This is unambiguously good news. Supply chain diversification reduces geopolitical risk, improves Apple’s bargaining power with TSMC on pricing, and strengthens the long-term resilience of Apple’s product engine. Nothing changes in the short term — but the 5-year risk profile improves meaningfully.

Holding TSM (TSMC):

The sky is not falling. TSMC keeps all of Apple’s flagship chips — M5 Pro, Max, Ultra, and every iPhone processor. Placing its least complex Mac-class SoC on a second source reduces single-foundry exposure without touching the flagship lines that rely on TSMC’s flagship silicon. However, a successful Intel Foundry signals real competition for the first time in years — which pressures TSMC’s long-term pricing power. Watch carefully.

Considering INTC:

The turnaround story is real. The technology is real. The government backing is real. But at 900x trailing earnings and a stock that has moved 170% in months, the easy money has been made. If you didn’t buy Intel when it was unloved and cheap, buying it at all-time highs after a parabolic move requires either exceptional timing skill or exceptional risk tolerance. Neither of which should be confused with investing.

Indian investor:

There is no direct way to buy INTC in India yet through most mutual funds. However, US tech ETFs and Nasdaq 100 funds (Motilal Oswal Nasdaq 100 FOF) give you indirect exposure to this semiconductor supercycle — including TSMC, Nvidia, and the AI chip buildout broadly. Check availability on your platform given SEBI overseas investment limits.

The Panther Lake Parallel: Intel vs Apple Silicon Head-to-Head

While all this plays out at the foundry level, there’s a second story running simultaneously.

Intel is not just building chips for Apple — it is still competing with Apple in the laptop market. And for the first time in years, the competition is genuine.

Intel’s Panther Lake architecture (Core Ultra Series 3), built on the 18A process, has finally closed the efficiency gap that made MacBooks untouchable on battery life for half a decade. Benchmarks from early 2026 show Panther Lake laptops matching MacBook Air battery performance in real-world workloads — something AMD and Qualcomm’s best chips have struggled to do consistently.

Apple’s M5 still holds the crown in single-core performance — the metric that determines how “snappy” everyday tasks feel. But Intel’s upcoming Nova Lake architecture, previewed for late 2026, is showing multi-threaded performance that matches or exceeds the base M5 in raw compute workloads.

For the first time since 2020, a Windows laptop powered by Intel is a legitimate alternative to a MacBook. That is a sentence that would have been laughable 18 months ago.

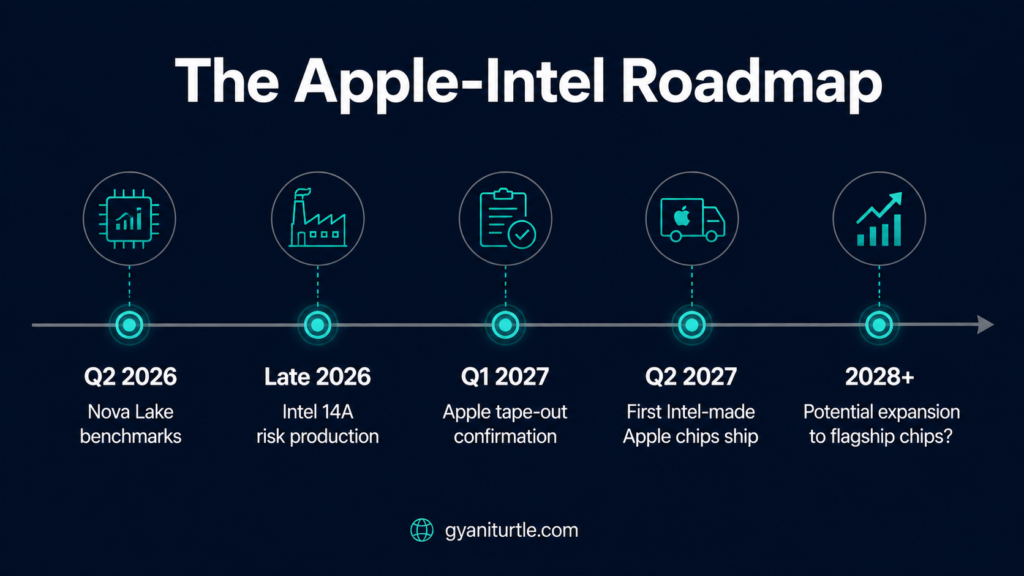

The Road Ahead: What to Watch

Q2 2026

Intel’s Nova Lake preview benchmarks — will it hold up at scale?

Late 2026

Intel 14A (1.4nm-class) risk production begins. If yields are credible, Intel enters a multi-year technology leadership window.

Q1 2027

Apple tape-out confirmation for 18A M-series chips. This is when the deal moves from analyst speculation to engineering reality.

Q2 2027

First Intel-manufactured Apple chips ship. The most important production milestone in the semiconductor industry in a decade.

2028 and beyond

Does Apple expand the Intel relationship to higher-tier chips? Does the success unlock Nvidia, Microsoft, and others as 18A customers? Does Intel achieve profitability?

These are the questions that will determine whether today’s 900x P/E was justified or whether it was the peak of a geopolitical hype cycle.

The Gyani Turtle Verdict

The Apple-Intel story is one of the genuinely fascinating narratives of 2026 — a story about technology, geopolitics, corporate strategy, and the slow, expensive rebuilding of American industrial capacity.

The technology is real. The deal is credible. The strategic logic on both sides is sound.

But the stock at 900x earnings is not an investment. It is a speculative position on perfect execution in a notoriously difficult industry. That is not the Gyani Turtle way.

Here is how a patient investor approaches this:

Use this story to understand the semiconductor landscape — which companies benefit from AI infrastructure buildout, which supply chains are becoming more resilient, and which geopolitical risks are being mitigated.

Consider broad exposure over single bets — US tech ETFs, Nasdaq 100 funds, or semiconductor ETFs give you the upside of this supercycle without betting everything on one company’s turnaround.

Watch the milestones, not the headlines — when Q2 2027 arrives and Intel ships its first Apple chips at scale, that is when the business thesis is confirmed. Until then, it is a story, not a result.

The divorce is over. The reunion is strategic, not sentimental. And the chips will decide who was right.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Are you holding INTC, AAPL, or TSM? Drop your take in the comments — we’d love to hear how global investors are positioning around this.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before making investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.

2 Comments