How to Save Tax Using ELSS Funds in India (2026 Guide)

The 30-Second Sip: ELSS — Equity Linked Savings Scheme — is the only Section 80C instrument that invests in equity, carries the shortest lock-in of just 3 years, and can save you up to ₹46,800 in tax annually at the 30% slab. But here is the trap that swallows thousands of Indian investors every March: if you are on the New Tax Regime — which has been the default since FY 2025-26 — ELSS saves you exactly zero tax. Section 80C deductions simply do not exist in the new regime.

This guide explains how to save tax using ELSS funds the right way: which regime you’re on, how the SIP approach beats the March lumpsum panic, how the 12.5% LTCG exit tax works, and the five mistakes that cost Indian investors lakhs every year.

This guide explains how to save tax using ELSS funds effectively, including tax benefits, SIP strategy, and common mistakes investors make.

Every March in India, something predictable happens.

A CA calls. A salary portal flashes a deadline. A WhatsApp group suddenly fills with tax-saving tips. And millions of salaried Indians rush to put ₹1.5 lakh somewhere — anywhere — before the financial year closes.

Most of that money goes into instruments that are safe, simple, and nearly useless for wealth creation. Tax-saver FDs at 7%. NSC at 7.7%. More PPF contributions on top of an already-locked corpus.

And every year, a smarter subset of investors quietly sets up an ELSS SIP in April — earns twelve months of equity returns, saves the same tax, and ends up significantly ahead.

The question is which investor you want to be.

But before we discuss how to save tax using ELSS funds, there is one critical question you must answer first.

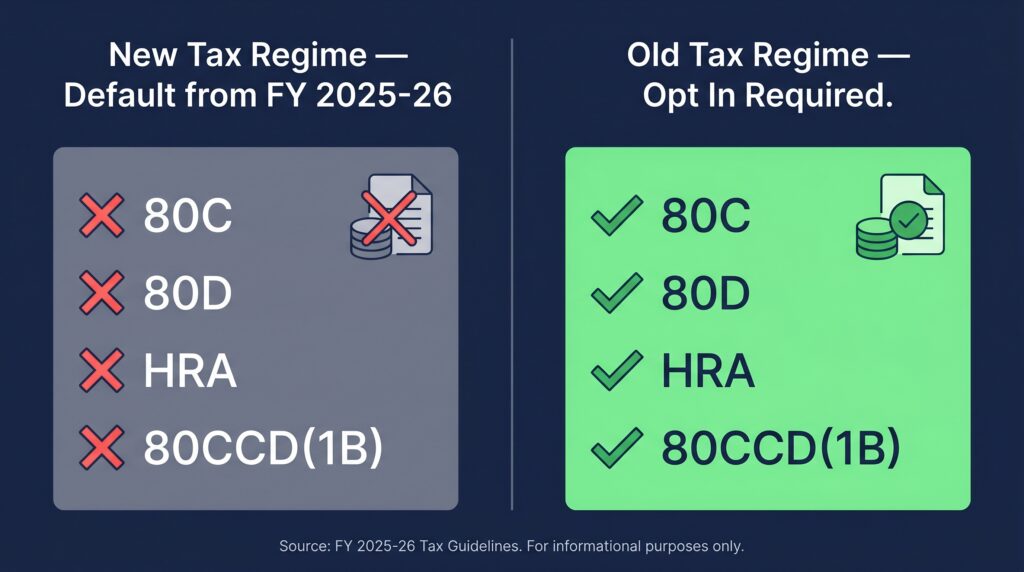

The Question Nobody Asks You First: Old Regime or New?

This is not a small detail. It is the foundational question that determines whether this entire article applies to you or not.

From FY 2023-24, the New Tax Regime is the default in India. Unless you actively opted for the Old Tax Regime during your employer’s investment declaration or in your ITR filing, you are almost certainly on the new regime.

And here is the consequence:

|

Tax Regime |

Section 80C Available? |

HRA Available? |

ELSS Tax Benefit? |

|---|---|---|---|

|

Old Tax Regime |

✅ Yes |

✅ Yes |

✅ Yes — up to ₹1.5 lakh |

|

New Tax Regime (Default) |

❌ No |

❌ No |

❌ Zero |

In the new tax regime, Section 80C deductions simply do not exist. No ELSS benefit. No PPF deduction. No NSC. No tax-saver FD. No home loan principal deduction. No life insurance premium deduction.

What the new regime offers instead is lower slab rates and a higher standard deduction of ₹75,000 — but no Chapter VI-A deductions at all.

An important correction: A common misconception circulates online — that the additional ₹50,000 NPS deduction under Section 80CCD(1B) is available in the new regime. It is not. From FY 2023-24 onwards, employee contributions to NPS under 80CCD(1B) are also not deductible under the new regime. Only the employer’s NPS contribution under Section 80CCD(2) remains deductible.

How to check which regime you are on:

- Look at your last salary slip — check which regime your employer is deducting TDS under

- Check your last ITR — it clearly states the regime chosen

- Ask your HR or payroll team directly

If you are on the new regime, ELSS remains a valid equity mutual fund worth investing in — but purely for wealth creation, not tax saving. The lock-in period and slightly higher expense ratios of most ELSS funds make them a less optimal choice compared to a plain index fund for pure investment purposes.

If you are on the old regime — read on. This guide is for you.

What Is ELSS? The Tax-Saving Mutual Fund Explained

ELSS stands for Equity Linked Savings Scheme. It is a mutual fund category that:

- Invests at least 80% of its corpus in equity and equity-related instruments

- Has a mandatory 3-year lock-in period from the date of each investment

- Qualifies for a Section 80C deduction up to ₹1,50,000 per financial year (old regime only)

Three numbers matter here:

3 years — the lock-in period. This is the shortest mandatory lock-in among all Section 80C instruments. PPF locks you in for 15 years. Tax-saver FDs for 5 years. NSC for 5 years. ELSS gives you your money back — potentially with substantial returns — in just 3 years.

80% — the minimum equity allocation. This is what gives ELSS its return potential and its volatility. It is not a debt instrument. Your corpus will fluctuate with the market during the lock-in period.

₹1,50,000 — the combined ceiling for all Section 80C instruments. If your EPF contribution, life insurance premium, and home loan principal repayment already consume this limit, additional ELSS investment yields no further tax deduction.

Understanding how to save tax using ELSS funds properly can help you avoid common mistakes

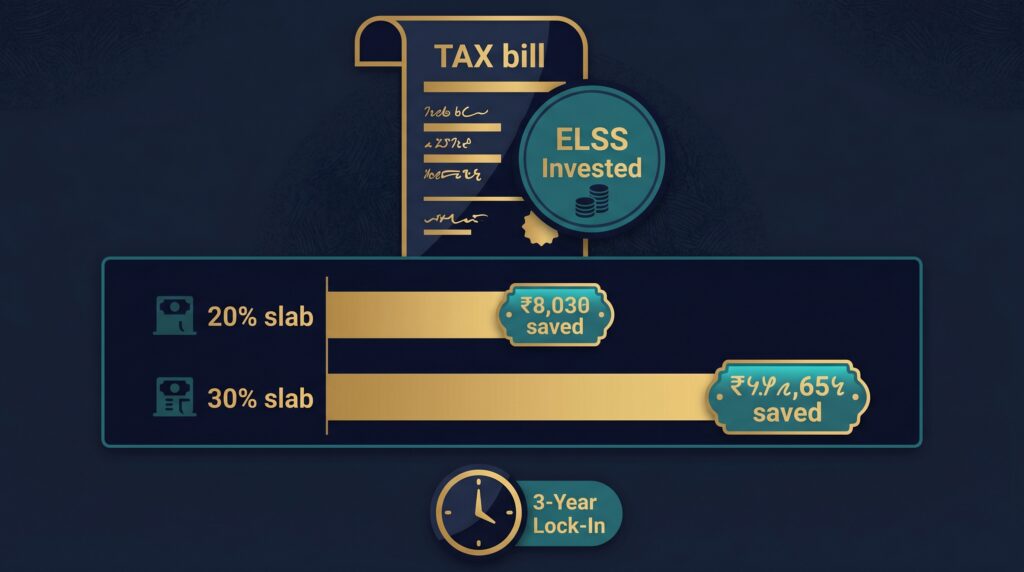

How to Save Tax Using ELSS Funds: The Numbers That Matter

The tax saving calculation from ELSS is straightforward. An 80C deduction reduces your taxable income by up to ₹1,50,000. The actual rupee saving depends on your income tax slab:

|

Your Tax Slab |

Maximum 80C Deduction |

Tax Saved (Incl. 4% Cess) |

|---|---|---|

|

20% income tax slab |

₹1,50,000 |

₹31,200 |

|

30% income tax slab |

₹1,50,000 |

₹46,800 |

These are guaranteed, immediate, real savings — delivered before the market has moved a single point on your investment.

The critical calculation before investing: Check how much of your ₹1,50,000 limit is already consumed.

Your 80C room = ₹1,50,000 − EPF employee contribution − Life insurance premium paid − Home loan principal repayment − School tuition fees (if applicable)

Only the remaining room after existing deductions creates additional tax saving through ELSS. If your EPF alone uses ₹90,000 of the limit, only ₹60,000 more of ELSS investment creates new tax benefit.

ELSS vs Every Other 80C Option: The Honest Comparison

|

Feature |

ELSS |

PPF |

Tax-Saver FD |

NSC |

|---|---|---|---|---|

|

Lock-in Period |

3 years |

15 years |

5 years |

5 years |

|

Return Type |

Market-linked (Variable) |

Fixed (Declared Quarterly) |

Fixed Contractual |

Fixed Compounded |

|

Risk Profile |

Market Volatility |

Sovereign Guarantee |

Bank Credit Risk |

Sovereign Guarantee |

|

Tax on Returns |

12.5% LTCG above ₹1.25L |

Completely tax-free |

Taxed at income slab |

Taxed at income slab |

|

Income Earned |

Nil (capital appreciation) |

Interest |

Interest |

Interest |

|

Growth Model |

✅ Equity compounding |

Debt Compounding |

Simple/Compounded Interest |

Compounded Interest |

Reading the table honestly:

ELSS wins on two counts: shortest lock-in and highest return potential. The 3-year lock-in means your capital is not frozen for a decade and a half like PPF.

PPF wins on one critical count: complete tax exemption at maturity (EEE status — exempt at investment, exempt on interest, exempt on withdrawal). If your horizon is 15 years and you never need the money, PPF’s tax efficiency is unmatched.

The Gyani Turtle recommendation for 80C allocation: Neither ELSS nor PPF alone. A combination — ELSS for equity compounding potential with the 3-year flexibility, PPF for guaranteed stable returns with full tax exemption — has historically served most old-regime investors better than either in isolation.

Two Investors, One Tax Season: The Right Way and the Wrong Way

This is a fictional educational scenario. Not investment advice.

Arjun Kapoor, Mumbai. Annual income: ₹18 LPA. Tax slab: 30%. FY 2025-26.

❌ The Wrong Choice — The New Regime Trap

Arjun’s HR department asks him to declare tax-saving investments in April. He ignores the declaration form because he doesn’t understand it and misses the old regime selection deadline. He defaults to the New Tax Regime.

In January, a friend mentions ELSS. Arjun puts ₹1.5 lakh into an ELSS fund in a panic.

What he gets: A 3-year-locked equity mutual fund investment. Good wealth creation potential. Zero tax saving — because 80C deductions don’t exist in the new regime. His TDS was already calculated at new regime rates.

The cost: Arjun effectively made an investment that is suboptimal for his situation. An index fund with no lock-in would have been better for pure investment purposes. The ELSS lock-in gives him nothing in return without the tax benefit.

✅ The Right Choice — April SIP in Old Regime

Arjun’s colleague Meera earns the same ₹18 LPA. In April, she visits her CA, confirms she should be on the Old Tax Regime given her HRA, home loan, and insurance premiums, and opts in explicitly through the employer declaration form.

She sets up a ₹12,500 per month ELSS SIP starting April — spreading ₹1.5 lakh across 12 instalments rather than deploying a lumpsum in March.

What she gets:

- ₹46,800 in immediate tax saving at her 30% slab

- 12 months of SIP-averaged cost — buying more units when markets fall, fewer when they rise

- Each instalment independently starts its 3-year lock-in from its purchase date

- No March panic, no timing risk, no lumpsum market-entry risk

The gap after 3 years: Meera’s April SIP, running through a full market cycle, has both the tax saving and the rupee-cost averaging benefit. Arjun has locked his money for 3 years for no tax benefit and missed the cost-averaging advantage of spreading his investment.

The difference between these two outcomes was one form, filled in April.

The ELSS Exit Tax: Understanding LTCG and STCG

This is where most ELSS articles give outdated or inaccurate information. Here are the current 2026 rules:

After the mandatory 3-year lock-in, on redemption:

- Gains up to ₹1,25,000 per financial year are completely tax-free (LTCG exemption)

- Gains above ₹1,25,000 are taxed at 12.5% LTCG (no indexation benefit)

Example: You invested ₹1,50,000. After 4 years it is worth ₹2,80,000. Your gain is ₹1,30,000. The first ₹1,25,000 is exempt. Only ₹5,000 is taxed at 12.5% — a tax of just ₹625. Highly efficient.

The SIP instalment complication: Each monthly SIP instalment has its own independent 3-year lock-in. If you start a ₹10,000/month SIP in April 2026:

- April 2026 instalment unlocks in April 2029

- May 2026 instalment unlocks in May 2029

- And so on through March 2027, which unlocks in March 2030

You cannot redeem the entire SIP corpus at once on the 3-year anniversary of your first instalment. The last 12 months of instalments are still locked when the first instalment becomes redeemable.

The 20% STCG penalty: If you somehow redeem within 1 year (which isn’t possible during the lock-in, but applies after it expires if you hold additional units or choose to redeem early after the lock-in): Short-Term Capital Gains are taxed at a flat 20% rate. There is no Rs 1.25 lakh exemption for STCG.

The Five Most Expensive ELSS Mistakes

Mistake 1: Investing in March as a Lumpsum

The classic error. Deploying ₹1.5 lakh as a single lumpsum in the last week of March means your entire corpus enters the market on one day at one price. If markets are near a peak that week — as they often are, driven by the same tax-season demand — your entry cost is high.

The fix: Start a ₹12,500/month SIP in April. Same annual investment, twelve entry prices, zero timing anxiety.

Mistake 2: Investing in ELSS While on the New Tax Regime

As explained above — this is the single most expensive mistake, costing the investor ₹31,200–₹46,800 in tax saving for which they have done the work of investing and locking in their money for 3 years with no benefit. Always confirm your regime before investing.

Mistake 3: Redeeming at Exactly 3 Years

Many investors treat the 3-year lock-in as the ideal exit date. It is not. ELSS is an equity fund. Equity delivers its best results over 5–10 years. Redeeming at the legal minimum lock-in date — just because you can — is leaving compounding on the table.

Mistake 4: Choosing Based on 1-Year Returns

The ELSS fund that returned 55% last year may have done so by taking concentrated risk in momentum-driven mid and small-cap stocks at peak valuations. The same approach that produced last year’s return can produce next year’s drawdown. Look at 5-year and 7-year rolling returns, consistency across multiple market cycles, and the fund manager’s risk management record.

Mistake 5: Buying the Regular Plan Instead of the Direct Plan

Every ELSS fund has two variants: Regular Plan (bought through a broker or distributor) and Direct Plan (bought directly from the AMC or through a direct-investment platform). The Regular Plan has a 0.5–1.5% higher annual expense ratio to pay the distributor’s commission. Over a 7-year holding period on a ₹1.5 lakh investment, this seemingly small difference can amount to a gap of ₹15,000–₹30,000 in final corpus value. Always choose the Direct Plan.

ELSS Funds Worth Knowing in 2026

These funds are mentioned for educational reference only. They are not specific recommendations. Always verify current expense ratios, portfolio composition, and track records on AMFI (amfiindia.com) before investing. Past performance does not guarantee future results. Consult a SEBI-registered adviser for personalised guidance.

For conservative ELSS investors (large-cap focused): Mirae Asset ELSS Tax Saver Fund — consistent portfolio construction, disciplined across market cycles, no excessive concentration.

For growth-oriented ELSS investors: Quant ELSS Tax Saver Fund — uses quantitative models, higher volatility profile, strong long-term numbers but not suitable for conservative risk tolerance.

For investors wanting international diversification: Parag Parikh ELSS Tax Saver Fund — unique for holding both Indian equity and international stocks. Adds geographic diversification uncommon among ELSS funds.

For large-cap comfort with ELSS benefits: SBI Long Term Equity Fund — India’s largest AMC backing, conservative positioning, suitable for investors uncomfortable with mid/small-cap volatility.

The one non-negotiable across all ELSS funds: Always select the Direct Growth variant — not Regular, not Dividend. Direct Plan + Growth option is the correct selection for every long-term ELSS investor.

Your ELSS Action Plan for FY 2026-27

Step 1 — Check your tax regime first Confirm with your CA or HR whether you are on the Old or New Tax Regime for FY 2026-27. If you are on the new regime, ELSS gives you no tax benefit — consider a plain Nifty 50 index fund with no lock-in instead.

Step 2 — Calculate your actual 80C room ₹1,50,000 minus (EPF employee contribution + life insurance premium + home loan principal). Only invest in ELSS up to the remaining room.

Step 3 — Choose Direct Plan, Growth option only Never accept the Regular Plan. Never choose a dividend option — it triggers an unnecessary tax event and reduces compounding.

Step 4 — Set up a monthly SIP from April — not a March lumpsum Divide your ELSS budget by 12 and automate a monthly SIP. Link it to your salary credit date. Put the form on autopilot and do not think about it again.

Step 5 — Hold for 5–7 years, not just 3 The 3-year lock-in is the legal minimum — not the optimal exit point. Equity rewards patience. Let the compounding work beyond the lock-in period.

Step 6 — Plan your redemptions tax-efficiently When you do redeem, stay aware of the ₹1.25 lakh annual LTCG exemption. Spreading redemptions across two financial years can double your effective exemption to ₹2.5 lakh if your gains are large.

The Gyani Turtle Verdict

How to save tax using ELSS funds is one of the most searched personal finance questions in India — and one of the most poorly answered. Most answers skip the regime question, ignore the SIP-vs-lumpsum timing problem, and treat ELSS as a March emergency rather than an April discipline.

Here is the complete Gyani Turtle framework:

- Check your regime before you do anything else — the entire tax-saving case for ELSS collapses under the new regime

- Calculate your real 80C room — don’t invest ₹1.5 lakh if ₹80,000 is already consumed by EPF and insurance

- Start in April, not March — SIP from April beats lumpsum in March on both cost-averaging and planning discipline

- Direct Plan only, always — the Regular Plan is a gift to your distributor, not to your wealth

- Hold longer than 3 years — the lock-in is not the finish line, it is the starting line for serious compounding

- Plan redemptions around the ₹1.25 lakh LTCG exemption — smart exit timing reduces your tax bill meaningfully

ELSS is not magic. It will not make you rich by saving ₹46,800 in one year. But over a decade of disciplined April SIPs, with the tax saving reinvested and the compounding left undisturbed, it has historically been among the most efficient combinations of tax saving and wealth creation available to Indian salaried investors under the old regime.

The turtle wins by starting in April and never stopping.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

❓ FAQ

Does ELSS save tax in the New Tax Regime? No. Section 80C deductions — including ELSS — are not available under the New Tax Regime. ELSS is only a tax-saving instrument under the Old Tax Regime.

Can I invest more than ₹1.5 lakh in ELSS? Yes. You can invest any amount. But the tax deduction under 80C is capped at ₹1,50,000 across all eligible instruments combined. Amounts above this cap receive no additional deduction benefit, though they continue to grow as a regular equity mutual fund investment.

How to save tax using ELSS funds effectively? You can save tax using ELSS funds under Section 80C by investing up to ₹1.5 lakh per year.

What happens if I need money during the 3-year lock-in? You cannot redeem ELSS units before the 3-year lock-in expires. There are no partial withdrawal provisions or emergency exit options. This is why maintaining a separate emergency fund in a liquid instrument before investing in ELSS is essential.

Is SIP better than lumpsum for ELSS? For most investors, yes. SIP spreads your entry cost across 12 market prices rather than one, reducing the risk of investing a large amount at a market peak. It also aligns with monthly salary cycles and removes the March deadline pressure.

Can I claim 80C for ELSS purchased in a previous year? No. 80C deductions apply only to investments made within the relevant financial year (April 1 to March 31). Last year’s ELSS investment was last year’s deduction.

Also read:

- How to Start Investing in India — 2026 Beginner’s Guide

- SIP vs Lumpsum: Which is Better for You?

- What Happens to Your SIP When Market Falls 40%?

- Flexi Cap Mutual Funds India 2026

- SEBI Stress Test: Is Your Small-Cap Fund Safe?

Final Disclaimer

This article is for educational and informational purposes only. It does not constitute financial, investment, legal, or tax advice. Market conditions and central bank policy expectations can change rapidly. All data cited is derived from publicly available sources including the Bureau of Labor Statistics, Bureau of Economic Analysis, Federal Reserve, CME Group, and Chicago Federal Reserve. Please conduct your own research and consult a qualified financial professional before making any investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.