India Data Centre Investments 2026: The Definitive Guide

The internet has plumbing. Most people never see it.The 30-Second Sip: India’s data centre capacity stood at 1.7 GW in 2025 and is projected to reach 3 GW by 2028, according to CBRE. But the more important story is how that capacity generates returns — and not all data centres are built alike. Colocation charges per rack. Hyperscale locks in 15-year Power Purchase Agreements with Microsoft, Amazon, and Google. Edge earns premium yields by solving the latency crisis in Tier-2 cities. Understanding the distinction between these three models is central to understanding India data centre investments 2026 — whether you are an MSME evaluating your cloud bill, or an investor studying the infrastructure behind the AI boom.

The Indian Government is subsidising AI compute at just ₹65 per GPU-hour — roughly one-third the global rate. And India’s regulatory architecture — the RBI’s hard localisation mandate for payment and financial data, combined with the DPDP Act’s power to instantly restrict cross-border data flows to blacklisted countries — has driven global hyperscalers to build domestic capacity as a strategic hedge against regulatory disruption. Both facts change the economics permanently.

Behind every UPI transaction, every real-time pharmaceutical cold chain alert, every AI-generated product recommendation on your phone — there is a physical building, somewhere in India, running at full power 24 hours a day, cooling rows of servers that never sleep.

In 2026, as India data centre investments 2026 reach an inflection point, the question of where that building is, who built it, and which revenue model funds it has become one of the most consequential questions in Indian infrastructure investing. India data centre investments 2026 are not a monolithic story of one asset class. They are three distinct business models — Colocation, Hyperscale, and Edge — each with different risk profiles, return structures, and relevance to different investors.

This post explains how each model works, what drives the returns, and why India’s overlapping regulatory architecture — from the RBI’s hard localisation rules to the DPDP Act’s cross-border risk framework — has fundamentally altered the economics of all three.

The Regulatory Architecture: Why Global Companies Are Building in India

Before examining the revenue models, it is essential to understand the regulatory environment that has made domestic India data centre investments 2026 a strategic imperative for global companies — and why that pressure is more durable than a single law can explain.

The picture is more layered than a blanket data localisation mandate. The structural demand is driven by three overlapping regulatory forces acting simultaneously.

The RBI’s Hard Localisation Mandate: The Reserve Bank of India maintains strict data residency requirements for payment system data. All financial transaction data, card payment records, and banking information must be stored exclusively on servers physically located in India. Given that India processed over 131 billion UPI transactions in FY25 alone, this single mandate creates a substantial, non-negotiable floor of domestic data centre demand for every bank, fintech platform, payment aggregator, and insurance company operating in India — with no regulatory ambiguity and no cross-border routing permitted.

The DPDP Act’s Regulatory Risk Framework: India’s Digital Personal Data Protection (DPDP) Act 2023 — contrary to earlier 2018 drafts — did not mandate blanket data localisation. Under Section 16(1), it adopted a “negative list” approach: personal data can flow freely outside India except to countries explicitly restricted by the Central Government via notification. This is a fundamentally different legal mechanism from a universal localisation requirement.

However, this distinction creates a different — and arguably more powerful — demand driver for domestic infrastructure. The Central Government can add any country to the restricted list at any point, instantly disrupting the cross-border data flows of every company routing Indian user data through that territory. For a global technology company with tens of millions of Indian users, a sudden blacklisting of a country hosting its primary data processing centres would cause catastrophic operational disruption if no domestic fallback exists.

Global hyperscalers are rational actors. They build Indian data centres not because the law compels them to store all data domestically today, but because maintaining domestic compute capacity eliminates their exposure to a regulatory risk event that could shut down their Indian operations with minimal warning. The capital expenditure on Indian infrastructure is, in part, a premium paid for regulatory optionality.

Sector-Specific Mandates: Beyond the RBI, sector regulators including SEBI and the Insurance Regulatory and Development Authority of India (IRDAI) maintain their own data residency requirements covering market infrastructure data, investor records, and insurance policy information. The cumulative effect of these sector-level mandates — applied across finance, capital markets, and insurance — means a significant share of India’s highest-value digital economy is subject to hard localisation requirements regardless of the DPDP Act’s general cross-border transfer framework.

The combined result of these three forces is structural domestic demand that no single law needs to mandate in its entirety. As Anshuman Magazine, Chairman and CEO of CBRE India, noted in May 2026: “The data centre story in India is no longer about potential but about execution at scale. The sector’s resilience and attractive return potential are establishing it as a primary focus for investors, with foreign capital playing a dominant role.”

The Transmission Chain: From AI Arms Race to Your Doorstep

Understanding how India data centre investments 2026 connect global technology trends to Indian households requires tracing the full mechanism.

Step 1 — The Architecture Shift: The global AI arms race forces hyperscalers — Microsoft, Google, Meta — to transition from standard cloud storage to high-density, liquid-cooled GPU clusters. A single modern AI training facility generates heat densities that traditional air-cooled data centres cannot manage. The physical architecture of data centres is being rebuilt from scratch.

Step 2 — The Regulatory Pressure: India’s regulatory architecture creates powerful demand for domestic compute through two parallel mechanisms. The RBI mandates hard localisation for all payment and financial data — a sector that covers a massive share of India’s highest-value digital activity. The DPDP Act 2023, operating on a “negative list” framework under Section 16(1), gives the Central Government power to instantly restrict cross-border data flows to any blacklisted country without notice. Global hyperscalers respond by building domestic data centre capacity as a strategic hedge: a local facility eliminates the risk of operational disruption from a sudden regulatory change that could otherwise make Indian user data processing impossible overnight.

Step 3 — The Capital Influx: Recognising the supply-demand gap — India generates 20% of global data but houses 3% of global capacity — sovereign wealth funds and private equity giants commit over $126 billion, scaling toward $180 billion, into Indian infrastructure real estate.

Step 4 — Revenue Model Bifurcation: To service this capital, Indian operators split their business models. Massive campuses are leased to hyperscalers on 15-year Power Purchase Agreements (PPAs). Simultaneously, agile “Neoclouds” lease GPU-as-a-Service to domestic startups and enterprises that need AI compute without owning hardware.

Step 5 — The Edge Expansion: 5G networks, precision agriculture IoT, smart city infrastructure, and real-time healthcare logistics all demand sub-10 millisecond latency — something no centralised Mumbai server farm can reliably deliver to a device in Lucknow or Jaipur. This forces the buildout of micro-Edge data centres of 8–10 MW in Tier-2 and Tier-3 cities.

Step 6 — The Portfolio Impact: Retail and institutional investors gain exposure to these infrastructure returns through data centre REITs, InvITs, and the equities of domestic conglomerates pivoting into tech infrastructure. The digital economy now has physical real estate — and that real estate generates yield.

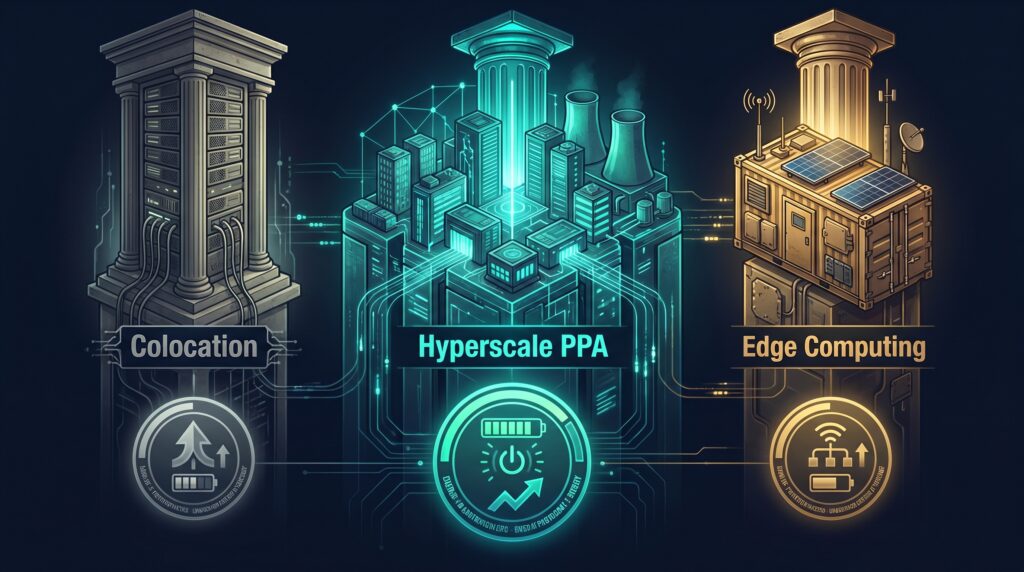

The Three Revenue Engines: How India Data Centre Investments 2026 Actually Make Money

This is the section most infrastructure coverage skips. Understanding the return mechanics of each model is essential context for any serious examination of India data centre investments 2026.

Model 1 — Retail Colocation: The Legacy Engine

Retail colocation is the original data centre business model. Operators build and maintain a secure, power-stable facility. Customers — typically Indian banks, IT firms, and enterprise software companies — lease individual racks or cages within that facility, paying for power usage, physical space, and bandwidth on a Service Level Agreement (SLA) basis.

The economics are straightforward: higher tenant count means higher revenue per square metre. The risk is tenant churn — enterprise customers can and do migrate their workloads to cloud as computing costs fall.

Historically, institutional analysts have tracked operator yields in the 12–15% IRR range for well-run retail colocation facilities. The growth trajectory for this model is slower globally as enterprises shift to cloud — but in India, where a large base of financial institutions and government entities require on-premise-equivalent security with outsourced facility management, retail colocation remains a substantial portion of the market.

The “Zombie” Risk: Critics note that the rapid shift toward liquid-cooled, high-density AI data centres is making older air-cooled colocation facilities obsolete faster than their 20-year depreciation schedules allow. Skeptics have coined the term “zombie data centre” for legacy Tier-2 facilities that lose hyperscale and enterprise tenants but remain as stranded assets on operator balance sheets. This is a genuine structural risk in India data centre investments 2026 that deserves honest acknowledgement.

Model 2 — Hyperscale (PPA): The Anchor Contract

The hyperscale model is architecturally and commercially different from colocation. An Indian operator builds a massive, purpose-designed facility — often 100 MW or larger — and leases the entire campus to a single hyperscaler (AWS, Microsoft, Google) under a long-term Power Purchase Agreement.

The financial characteristics of this model are distinctive: lower margin per megawatt than colocation, but near-zero vacancy risk. Moody’s and S&P have taken to describing these 15-year PPAs as quasi-sovereign credit given the elite corporate credit profiles of Microsoft and Amazon. The tenant is essentially paying rent on a building for 15 years regardless of short-term technology cycles.

For India data centre investments 2026, this model represents the bulk of the $67.5 billion in hyperscaler pledges (AWS: $35 billion, Microsoft: $17.5 billion, Google: $15 billion). The operator yield for hyperscale PPAs — historically 10–13% IRR — is lower than colocation, but the duration and credit certainty appeal to institutional investors and pension funds seeking predictable long-term cash flows.

Model 3 — Edge Computing: The High-Premium Frontier

Edge computing is the fastest-growing sub-segment of India data centre investments 2026 — and the least understood by most retail investors.

Rather than building centralised 100 MW campuses, Edge operators deploy compact, containerised units of 8–10 MW in Tier-2 and Tier-3 cities — right-sized facilities positioned close to end users to deliver sub-10 millisecond latency. The economic driver is premium: customers in healthcare logistics, precision agriculture, smart manufacturing, and autonomous vehicle testing cannot tolerate the 80–150 millisecond round-trip latency of a centralised Mumbai server farm.

India’s Edge data centre capacity stood at 80–100 MW in 2025 and is projected to expand to 160–180 MW by 2028 according to ICRA. The operator yield for premium Edge deployments — historically 18–22% IRR — reflects the latency premium and the fragmented, high-margin nature of Edge customers.

The risk profile is correspondingly higher: Edge requires fragmented land acquisition across multiple Tier-2 cities, grid reliability in markets where power consistency is variable, and the operational complexity of managing dozens of small sites rather than one large campus.

|

Feature / Metric |

Retail Colocation |

Hyperscale (PPA) |

Edge Computing |

|---|---|---|---|

|

India Context |

Per-rack leasing for banks and IT firms |

15-year locked campus contracts in Mumbai/Chennai |

8–10 MW containerised units in Tier-2 cities |

|

Revenue Model |

SLA-based: power, space, bandwidth |

Wholesale: fixed real estate lease + power pass-through |

Premium micro-leases driven by 5G and IoT latency |

|

Global Benchmark |

Slowing globally as cloud migrates |

Dominates 55%+ of global DC construction pipelines |

Fastest-growing sub-sector globally (CAGR >25%) |

|

Operator Yield (IRR) |

12–15% |

10–13% (lower margin, zero vacancy risk) |

18–22% (latency premium) |

|

Risk Level |

Medium (tenant churn) |

Low (quasi-sovereign credit tenants) |

High (fragmented land, grid reliability) |

All IRR figures are historical analyst estimates. Past performance and projected returns do not guarantee future outcomes. Actual returns vary significantly based on construction timelines, power costs, occupancy, and macroeconomic conditions.

The Arjun Story: Three Seconds That Cost ₹25 Lakhs

This is an illustrative scenario showing how India data centre investments 2026 affect real MSME decisions. Educational purposes only. Not investment advice. All figures are approximate and for illustration only.

Arjun (42), Pune, Maharashtra. Founder of a healthcare logistics and tracking firm. Business revenue: ₹2.5 Crores. His platform tracks temperature-sensitive pharmaceuticals across Maharashtra in real time.

❌ The Wrong Choice — Legacy Retail Colocation

Arjun hosts his real-time tracking infrastructure on a legacy Mumbai retail colocation facility. He pays standard enterprise rates — billed on peak data ingress and egress — with no long-term volume lock-in. The legacy air-cooled facility charges a premium for power inefficiency.

Annual cost: ₹83,00,000 (approximately $100,000).

During peak fleet movement windows, the legacy facility’s latency spikes to 3 seconds. Three seconds is imperceptible to a human. For a pharmaceutical cold chain system, it is the difference between catching a temperature drop in a vaccine storage unit and missing it entirely. A single missed alert spoils a ₹25,00,000 batch of vaccines.

National impact: Arjun’s dollar-linked hosting costs contribute to the Current Account Deficit. His vendor is a legacy facility with no green energy certification, consuming expensive grid power at rates above ₹7 per kWh.

✅ The Right Choice — Edge Computing + Neocloud + Government Subsidy

Arjun migrates his real-time IoT tracking nodes to a localised Edge data centre outside Pune. He shifts his core predictive routing algorithm to a domestic Neocloud provider and accesses the Indian Government’s subsidised AI compute framework at ₹65 per GPU-hour — approximately one-third the global market rate — to run his temperature-prediction model.

Annual cost: ₹37,35,000 (approximately $45,000).

Latency drops to sub-10 milliseconds. Temperature alerts are instantaneous. The ₹25,00,000 spoilage risk is eliminated. Arjun saves over ₹45,00,000 annually and reinvests the savings into hiring two biomedical engineers.

National impact: Arjun’s rupee payments circulate domestically. The Edge facility runs on a green power purchase agreement. His GPU compute costs support the government’s IndiaAI compute infrastructure.

The difference between these two businesses is not capital, technical expertise, or sector knowledge. It is awareness of infrastructure options that became available in 2025–2026.

The Power Arithmetic: Why Location Inside India Matters

One aspect of India data centre investments 2026 that receives almost no retail coverage is the power tariff arbitrage across Indian states — and it has a direct bearing on operator economics.

India’s inter-state industrial power tariff varies from ₹4.50 to ₹7.20 per kWh depending on the state, grid access, and renewable energy sourcing. For a 50 MW data centre facility, this differential translates to an annual operational cost difference of approximately $15 million between the cheapest and most expensive power markets in India, according to Mordor Intelligence’s 2026 India DC report.

This is why the geography of India data centre investments 2026 is not random. Operators are targeting states with favourable industrial power policies, proximity to green energy corridors, and access to reliable grid infrastructure — not just states with available land near large cities. The power tariff decision made at site selection stage can determine whether a facility is profitable or marginal for its entire operating life.

What the Government Is Building: IndiaAI, SHANTI, and the Nuclear Data Centre

India’s government is not merely a regulator of India data centre investments 2026 — it is an active co-builder of the underlying infrastructure.

IndiaAI Mission: The government has onboarded 38,231 GPUs at a subsidised rate of ₹65 per GPU-hour — approximately one-third the global average cloud rate. This compute is available to Indian startups, researchers, and enterprises through a domestic AI marketplace, directly reducing the cost of AI development in India without requiring investment in private GPU hardware.

Power Planning: Union Minister of State for Electronics and IT Jitin Prasada stated at a Rajya Sabha submission in March 2026: “Electricity demand from data centres is estimated to reach 13.56 GW by 2031–32.” To contextualise that figure: India’s total current installed power capacity is approximately 950 GW. Data centres alone are projected to consume 1.4% of total national power generation within six years. https://sansad.in

The SHANTI Act: Recognising that renewable energy alone cannot reliably power high-density, 24/7 AI data centres, the Ministry of Electronics and IT is advancing the SHANTI (Sustainable High-capability AI and Nuclear Technology Infrastructure) Act — a policy framework to integrate small modular nuclear reactors (SMRs) as a stable baseload power source for AI infrastructure. This is an emerging policy development and its implementation timeline remains uncertain, but it signals the government’s long-term commitment to the power infrastructure required for large-scale India data centre investments 2026 and beyond.

SEBI’s Regulatory Role: SEBI has progressively strengthened the regulatory framework for InvITs and REITs — enhancing transparency, improving credit access, and enabling operators to monetise existing data centre assets and recycle capital into new builds. This regulatory evolution is what makes it possible for retail capital to eventually access the returns generated by this infrastructure.

In-body disclosure: MeitY, SEBI, Moody’s, S&P, CBRE, Avendus Capital, ICRA, and Mordor Intelligence are referenced as institutional data sources only. This does not constitute a recommendation related to any entity mentioned.

The Honest Counter: What the Critics Say Correctly

At Gyani Turtle, we never oversell. The structural thesis behind India data centre investments 2026 is compelling — but the critics raise concerns that belong in every honest analysis.

Geographic Concentration: The current 3 GW development pipeline is heavily concentrated in Mumbai and Chennai. Both cities already face peak-summer power grid strain and water table stress. Data centres are among the most water-intensive industrial users — a single hyperscale facility can consume millions of litres of water annually for cooling. IMF and World Bank assessments have consistently flagged the carbon and water footprint of hyperscale facilities in water-stressed regions as a structural governance risk.

The “Zombie Data Centre” Problem: The rapid transition to liquid-cooled, high-density AI facilities is making older air-cooled colocation infrastructure obsolete faster than projected depreciation schedules. Legacy Tier-2 facilities losing enterprise tenants to cloud migration — but unable to attract hyperscale clients due to insufficient power density — may become stranded assets on operator balance sheets. This risk is not theoretical; it has already played out in the US market.

The Hardware Cycle Risk: The entire high-IRR projection for GPU data centres rests on continued enterprise demand for generative AI compute. If the revenue from AI software products does not scale fast enough to justify the $25,000+ price tag of Nvidia H100 GPUs, hyperscalers may reduce expansion commitments. Indian developers who front-loaded capital expenditure for “Build-to-Suit” shells could face a commercial real estate stress cycle if anchor tenants delay or reduce their footprints.

The Commitment vs Deployment Gap: $180 billion in investment “pledges” is not $180 billion deployed. Land acquisition, green power purchase agreements, and state-level regulatory approvals have historically extended Indian infrastructure timelines by 2–4 years. Actual facility operations — and the cash flows that generate investor returns — lag commitments by a material period.

These risks do not invalidate the structural thesis. They define the boundaries within which it operates.

How Different Market Participants Evaluate India Data Centre Investments 2026

Salaried professionals and long-term equity investors: Market participants tracking India data centre investments 2026 have historically examined this theme through two lenses. The first is direct infrastructure exposure — SEBI-regulated InvITs and REITs that hold data centre assets, offering yield-generating instruments with physical asset backing. The second is indirect equity exposure through publicly listed real estate developers and conglomerates pivoting into tech infrastructure parks.

Analysts have noted that the asset class’s cyclicality, long construction timelines, and power dependency make it better understood as a thematic complement to — rather than a replacement for — core equity index exposure.

MSME business owners and operators: India’s MSME ecosystem is increasingly examining its cloud architecture in light of the new infrastructure landscape. Businesses running IoT-dependent operations — healthcare logistics, precision agriculture, smart manufacturing, real-time fleet tracking — are evaluating the cost and latency case for migrating from centralised cloud providers to domestic Edge facilities. The government’s ₹65-per-GPU-hour subsidy framework is particularly relevant for MSMEs running AI-intensive workloads that were previously cost-prohibitive on global cloud platforms.

Retail investors and individual savers: Analysts studying the “picks and shovels” of the AI infrastructure buildout have documented interest in the ancillary supply chains that every data centre facility requires regardless of which operator wins the market. Industrial cooling systems, heavy electrical transformers, optical fibre networks, and green energy generation are sectors that have historically attracted interest during large-scale infrastructure build cycles. Retail investors examining India data centre investments 2026 have studied these adjacents as a way to gain thematic exposure with somewhat more diversified risk than direct data centre asset ownership.

NRIs and globally mobile Indians: NRIs can access data centre-related REITs and InvITs through NRE or NRO accounts under the Portfolio Investment Scheme (PIS). The distribution structures of InvITs typically comprise a mix of dividend, interest income, and return of capital — each with different tax treatment. Interest income is taxed at applicable rates, while return of capital is generally not taxed at the time of distribution.

NRIs investing via NRO accounts should note that DTAA benefits must be actively claimed to prevent maximum TDS deductions; the applicable DTAA depends on the country of residence and varies significantly. Currency risk is an additional consideration: because hyperscaler leases are denominated in INR, long-term rupee depreciation against the dollar can erode the real yield for NRIs repatriating returns to USD or GBP.

Families managing long-horizon portfolios: Multi-generational wealth managers have historically studied large infrastructure build cycles through the lens of resource scarcity alongside asset creation. The data centre boom is notable for its demand on two underpriced resources: electricity and water. Long-horizon portfolio managers have begun examining the intersection of green energy generation, industrial water management, and digital infrastructure as a structural allocation theme — recognising that the physical inputs to AI are as important as the digital outputs.

The Gyani Turtle Verdict

India data centre investments 2026 are not a single story. They are three distinct business models — Colocation, Hyperscale, and Edge — each operating at different scales, risk profiles, and return structures. Understanding which model a specific facility or operator uses is the foundational question before any further analysis.

What has changed structurally in 2026 is not the existence of data centres — it is the confluence of three forces that together make the investment thesis more durable than it was in 2022 or 2023:

The DPDP Act has created a regulatory floor that removes optionality from global companies. They must be in India. The question is no longer whether they build Indian data centres; it is how fast.

The government’s ₹65-per-GPU-hour subsidy has made domestic AI compute accessible to Indian MSMEs and startups at a price point that was previously available only to large enterprises or those with offshore infrastructure budgets.

And the power arithmetic — a $15 million annual cost difference for a single 50 MW plant based solely on state power tariff selection — means that disciplined operators with intelligent site selection will earn structurally higher returns than those who simply build wherever land is cheapest.

Here is the Gyani Turtle framework for thinking about this theme:

- Know the model — Colocation, Hyperscale, and Edge have fundamentally different return structures and risk profiles; treat them as distinct asset sub-classes

- Understand the regulatory architecture — the RBI’s hard localisation mandate for financial data, combined with the DPDP Act’s power to blacklist cross-border data flows, creates structural domestic demand that does not depend on blanket localisation to be durable

- The power question is central — state-level power tariff and renewable energy access determine long-run operator economics more than any other single variable

- The zombie risk is real — legacy air-cooled colocation facilities face structural obsolescence as liquid-cooled AI infrastructure scales; this is a genuine stranded-asset risk in portions of the market

- Commitments are not cash flows — $180 billion in pledges will deploy over years, not months; the gap between announcement and first revenue is the primary execution risk

- IRR projections are analyst estimates — the 25.5–28% equity IRR figures from Avendus Capital represent projected hold-to-maturity outcomes at current capex and pricing levels; they are not guaranteed returns

Through India data centre investments 2026 and beyond, India is building the physical infrastructure of its digital future — server by server, rack by rack, edge node by edge node. That process is slow, capital-intensive, and complicated. It is also structurally inevitable.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Also read:

- India’s $180B Data Center Boom: The 2026 AI Investment Guide

- How to Use Agentic AI in Investment and Trading — A Complete Guide for Indian Investors

- Is Your TCS SIP Safe? 5 Truths About AI and India’s IT Stocks in 2026

- The White Collar Recession Nobody Is Talking About

- How to Start Investing in India as a Beginner (2026 Complete Guide)

⚠️ EDUCATIONAL CONTENT ONLY

Gyani Turtle is NOT a SEBI-registered Investment Adviser (RIA) or Research Analyst (RA), and is not a licensed financial adviser in any jurisdiction globally. This article is written for general financial education and awareness only. Nothing in this article constitutes personalised investment advice, a solicitation, or a recommendation to buy or sell any security, fund, or financial instrument in any market.

SEBI has clarified that disclaimers alone do not protect unregistered content creators if the substance of the content constitutes investment advice. This blog is structured to remain strictly within the bounds of financial education — explaining concepts, mechanisms, and historical patterns — and does not provide specific buy/sell/hold recommendations on any individual security.

Availability of financial instruments discussed may vary by jurisdiction. Tax treatment, regulatory access, and legal status of instruments differ across countries.

Please consult a SEBI-registered Investment Adviser, AMFI-registered Mutual Fund Distributor, or a licensed financial professional in your jurisdiction before making any investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.