Stagflation Definition Impact & Investment Strategy Guide 2026

The 30-Second Sip: In the vast vocabulary of economics, one word strikes genuine terror into the minds of central bankers and fund managers alike — and it is not “recession.” It is stagflation. The stagflation definition is precise: simultaneous economic stagnation and persistent inflation. As of mid-2026, the US is displaying exactly this pattern. GDP growth slowed to a revised 1.6% in Q1 2026, while the Federal Reserve’s preferred inflation gauge — the PCE Index — accelerated to 3.8%. This is not a coincidence.

It is a structural paradox that places the Fed in a double bind: raise rates to fight inflation and choke economic growth further; cut rates to support growth and pour fuel on the inflationary fire. This guide covers the complete stagflation definition, impact, and investment strategy framework a patient investor needs to understand in 2026.

In the vast lexicon of economics, one word strikes genuine terror into the hearts of policymakers and seasoned fund managers alike. Not “recession.” Not “bubble.” The word is stagflation.

For several years, retail investors operated under a relatively predictable economic narrative: central banks raise rates to cool a post-pandemic consumption boom, inflation subsides, rates glide back down, and economic expansion continues. The stagflation definition impact, and investment strategy implications were considered historical footnotes — something studied in the context of the 1970s oil shocks, not a live threat to a 21st-century diversified portfolio.

As we advance through mid-2026, that comfortable narrative has been shattered. The latest figures from the Bureau of Economic Analysis reveal a dangerous dual trend. US GDP growth slowed dramatically to an inflation-adjusted annual rate of 1.6% in Q1 2026, down from the 2.1% recorded in 2025 — while the PCE index accelerated to 3.8%. Understanding the full stagflation definition impact, and investment strategy response is no longer an academic exercise. It is an operational necessity for any serious investor.

What Is Stagflation? Definition, Causes and Why It Matters

The stagflation definition that every investor must internalise is built from two economic forces that are not supposed to exist simultaneously:

Stagnation: Economic growth slowing below trend, characterised by rising unemployment, flat or declining corporate revenues, and falling consumer confidence.

Inflation: A persistent rise in the price level across goods, services, and assets — eroding the real purchasing power of money even as the economy weakens.

The reason stagflation is so structurally dangerous is that it violates a foundational assumption baked into the design of modern central banking: that high inflation accompanies high growth, and slow growth accompanies low inflation. These two pathological conditions — stagnation and inflation — were historically assumed to be mutually exclusive. When they arrive together, the policy tools available to central banks become not just ineffective but actively counterproductive.

The 2026 data is not ambiguous about where the global economy sits relative to the stagflation definition:

|

Economic Signal |

Current Reading |

Target / Benchmark |

Assessment |

|---|---|---|---|

|

US GDP Growth (Q1 2026) |

1.6% annualised |

2.0–2.5% trend growth |

⚠️ Below trend |

|

Headline PCE Inflation (April 2026) |

3.8% |

2.0% Fed target |

❌ Well above target |

|

Core PCE Inflation (April 2026) |

3.3% |

2.0% Fed target |

❌ Above target, rising |

|

NY Fed Inflation Gauge (April 2026) |

4.0% |

N/A |

❌ Elevated |

Source: Bureau of Economic Analysis / Federal Reserve, April–May 2026

The combination of sub-trend GDP growth and above-target, accelerating inflation is the textbook stagflation definition applied to real 2026 data. This is not a theoretical risk being hedged against — it is the measurable current environment.

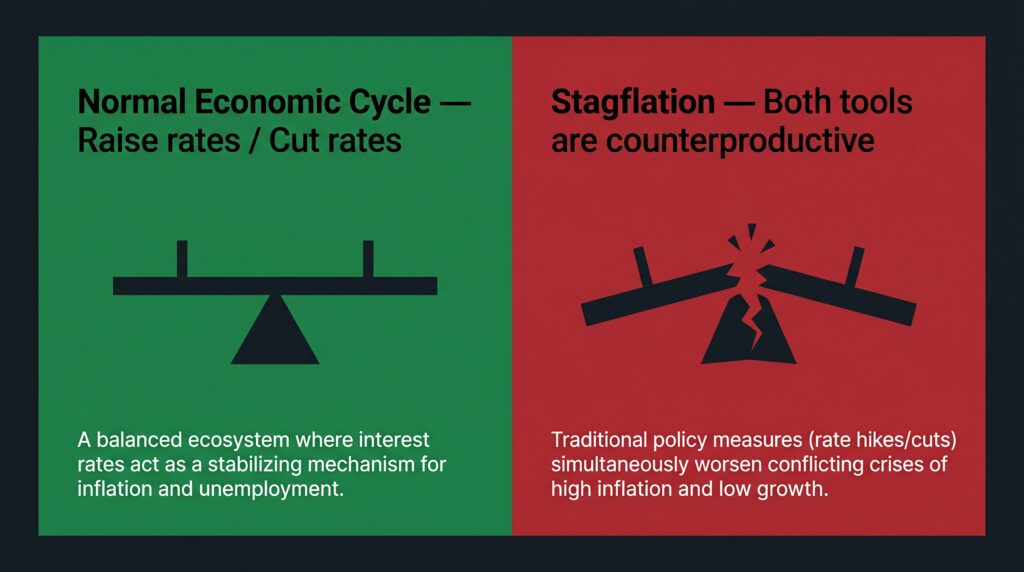

The Fed’s Double Bind: How the Dual Mandate Breaks Under Stagflation

To understand why the stagflation impact on monetary policy is so severe, one must look at the legal framework governing the Federal Reserve. The Fed operates under a Dual Mandate established by Congress:

- Price Stability — maintaining inflation at approximately 2%

- Maximum Employment — supporting sustainable economic growth and job creation

In a normal economic cycle, these two goals function like a balanced seesaw. Economic overheating drives inflation up; the Fed raises rates to cool it, restoring balance. A slowdown drives unemployment up; the Fed cuts rates to stimulate hiring, restoring balance.

Stagflation breaks the seesaw completely.

When slowing growth (1.6% GDP) and rising inflation (3.8% PCE) occur simultaneously, the Fed’s tools produce opposite effects on each mandate:

- If the Fed raises rates to crush the 3.8% inflation: higher borrowing costs will choke off the remaining economic growth, likely driving unemployment higher and risking a formal recession. The growth mandate is sacrificed.

- If the Fed cuts rates to rescue the sluggish 1.6% GDP: cheap credit will encourage further spending and allow the energy-driven inflation shock to entrench itself structurally in the economy. The price stability mandate is sacrificed.

As Mark Zandi, Chief Economist at Moody’s Analytics, summarised in recent commentary: the economy “isn’t just soft, it’s struggling” — with corporate margins under pressure and real household incomes shrinking due to high prices. The stagflation impact on policy effectiveness is not partial — it is total. Every available lever makes at least one half of the problem worse.

How Stagflation’s Impact Spreads Across Global Markets

The stagflation impact is not confined to the domestic US economy. Because the US Dollar functions as the global reserve currency, a stagflationary environment in Washington transmits itself to global markets through three distinct macroeconomic channels:

Channel 1 — The Corporate Margin Squeeze: International companies across manufacturing, technology, and consumer goods rely on global supply chains for components and raw materials. In a global stagflationary environment, the cost of imported inputs remains high due to persistent inflation. Simultaneously, because growth is slowing, end-consumers reduce discretionary spending. Exporters face higher input costs alongside shrinking sales volumes — a direct squeeze on corporate profit margins that flows into equity valuations worldwide.

Channel 2 — The Risk-Off Capital Flight: When global institutional investors recognise that the world’s largest economy is entering a stagflationary phase, risk tolerance contracts sharply. Capital exits growth-oriented emerging markets and speculative sectors and migrates to safe-haven assets. This outflow creates broad selling pressure on international equity indices, generating volatility that affects retail portfolios far from the source of the stagflationary signal.

Channel 3 — Imported Inflation and Policy Constraints: Most countries are net importers of crude oil and industrial metals. If the global energy shock remains elevated — as the structural analysis in the US-Iran ceasefire piece demonstrates — international economies absorb imported stagflation directly. Elevated energy costs push wholesale and retail inflation higher worldwide, forcing international central banks to maintain restrictive monetary policy even when their own domestic growth data would normally argue for easing.

Two Portfolios, One Stagflationary Storm

This is a fictional educational scenario. Not investment advice. All figures are illustrative only.

Priya and James both manage diversified global portfolios of comparable size, starting mid-2026 with the same economic data available to both.

Priya’s approach — Unadjusted Growth Portfolio: Priya maintains heavy exposure to small-cap and high-growth technology equities, reasoning that the economy will eventually recover and that her 5-year horizon absorbs short-term volatility. She holds long-duration bond funds expecting rate cuts to materialise within six months. She has no meaningful allocation to gold or short-duration instruments.

As the stagflation environment deepens over subsequent quarters: small-cap equities with high debt levels face refinancing pressure from sustained elevated rates. Long-duration bond NAVs erode as the anticipated rate cuts fail to arrive. Priya’s portfolio experiences simultaneous drawdowns in both equity and fixed income components — the classic stagflation trap for investors positioned for a straightforward rate-cut cycle.

James’s approach — Defensive Stagflation Posture: James reads the stagflation signals in the GDP and PCE data and restructures toward what market historians identify as stagflation-resilient positioning. He rotates toward large-cap companies with demonstrated pricing power, increases short-duration debt exposure to capture high yields without duration risk, maintains a dedicated gold allocation as structural inflation insurance, and holds a six-month liquid cash buffer.

During the same period of market stress: his large-cap holdings demonstrate relative earnings resilience as pricing power protects margins. His short-duration instruments capture the high-yield environment without capital erosion. His gold allocation performs as an inflation hedge. His cash buffer is available for opportunistic deployment when equity valuations correct.

The divergence between these two portfolios is not explained by different market access or different risk tolerance. It is explained by the recognition — or non-recognition — of the specific economic environment defined by the stagflation data.

A Defensive Investment Strategy Matrix for Stagflation

Historical studies of stagflationary cycles — the 1970s oil shock era being the most extensively documented — consistently show that the portfolio composition strategies that delivered strong returns during normal growth cycles require significant adjustment. The following matrix captures the patterns that institutional and academic analysts have historically observed:

|

Asset Class |

Behaviour in Stagflation Environments |

Observed Historical Role |

Typical Market Participant Approach |

|---|---|---|---|

|

Large-Cap / Blue-Chip Equities |

Moderately resilient — multinational companies with strong brand equity can pass input cost inflation to consumers |

Foundational equity base with pricing power buffering margin compression |

Maintained as core equity anchor with tilt toward value over pure growth |

|

Small-Cap / High-Growth Equities |

High vulnerability — smaller companies lack cash reserves to absorb sustained high borrowing costs and squeezed margins |

Elevated short-term volatility; earnings forecasts frequently cut |

Reduced allocation; restricted to long-horizon, cost-averaging positions only |

|

Short-Duration Debt / T-Bills |

Strong performer — delivers predictable, high nominal returns without exposure to duration-driven capital loss |

Provides income without interest rate risk |

Increased weighting to lock in current elevated yields |

|

Gold and Precious Metals |

Historical standout performer — thrives during currency debasement, persistent inflation, and geopolitical friction |

Structural portfolio insurance; non-correlated to equities in crisis |

Maintained as dedicated strategic allocation to hedge inflation purchasing power loss |

|

Cash and Liquid Reserves |

Essential optionality — preserves purchasing power and deployment capacity when equities correct |

Enables opportunistic buying at discounted valuations |

Increased to create financial buffer for household expenses and investment opportunities |

Note: The patterns above are drawn from academic and institutional historical studies of past stagflation cycles. Past patterns do not guarantee future asset class performance. This table is educational and does not constitute a personalised allocation recommendation.

How Financial Planners Approach Stagflation-Resilient Portfolio Construction

Note: The following describes historical financial planning approaches for educational purposes.

Academic literature and institutional research on stagflation consistently highlight three foundational principles that financial planners across disciplines have applied during stagflationary environments:

Building a Liquid Emergency Reserve: In stagflationary cycles, corporate profitability faces sustained headwinds that can occasionally translate into workforce restructuring and hiring slowdowns across exposed sectors. Financial planners consistently emphasise the importance of a liquid reserve — covering multiple months of core household expenses — parked in risk-free, immediately accessible instruments. The critical distinction is that this buffer is not an investment vehicle; its sole purpose is capital preservation and instant availability during economic uncertainty.

Eliminating Variable-Rate, High-Cost Liabilities: With inflation remaining structurally above target, central bank rates are unlikely to decline rapidly. Financial advisers across jurisdictions have historically highlighted the priority of reducing variable-rate debt — credit card revolving balances, floating-rate personal loans, adjustable-rate mortgages — before that debt becomes more expensive as rate conditions remain elevated. The mathematical certainty of compounding interest at current rates makes liability management as important as asset allocation during a stagflationary regime.

Rotating Equity Exposure Toward Pricing Power: The historical record of stagflation-era equity performance consistently distinguishes between companies that can maintain earnings through an inflationary period and those that cannot. Analysts define pricing power as the ability to raise product or service prices to offset input cost increases without losing meaningful market share to competitors. Academic studies of the 1970s stagflation cycle show that dominant consumer staples, utility providers, and essential healthcare companies demonstrated significantly more resilient earnings relative to discretionary and highly leveraged sectors.

The Gyani Turtle Verdict

The stagflation definition impact, and investment strategy challenge of mid-2026 is not a distant historical curiosity. It is the current operating environment, confirmed by hard data: GDP at 1.6%, PCE at 3.8%, Core PCE still rising at 3.3%, and a Federal Reserve with every policy lever producing trade-offs rather than solutions.

The word “stagflation” generates fear precisely because it exposes the limits of the tools that central banks have successfully used to manage the economy for decades. Those tools work when growth and inflation move in predictable tandem. When they diverge — stagnation in one direction, inflation in the other — the seesaw breaks.

But for the patient investor, a macro double bind is not a reason to exit markets or abandon long-term wealth-building strategies. It is an invitation to introduce structural maturity into portfolio construction. The historical evidence from past stagflation cycles consistently shows three things:

- Long-duration fixed income underperforms — duration risk is the specific mathematical hazard of a higher-for-longer rate environment, and it is avoidable

- Quality equities with pricing power outperform cyclical and leveraged peers — the divergence is large and historically consistent across stagflation episodes

- Gold and real assets provide portfolio insulation — not as speculation but as structural inflation insurance against currency purchasing power erosion World Gold Council — Gold in portfolios

The 2026 data does not guarantee a repeat of the 1970s. But it confirms that the preconditions for stagflation are present and measurable. Investors who understand the stagflation definition, impact, and investment strategy framework, and who adjust their portfolio construction accordingly, position themselves to weather this environment without panic — and to deploy capital opportunistically when valuations eventually reflect the macro headwinds.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Also read:

- US-Iran Peace Deal: Inflation Impact on Rate Cuts in 2026

- Market Volatility: 3 Reasons Indian Investors Shouldn’t Panic

- SIP vs Lumpsum: Which is Better for You?

- What Happens to Your SIP When Market Falls 40%?

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.