SEBI Mutual Fund Stress Test: Is Your Small-Cap Fund a Liquidity Trap?

There is froth in small and mid-cap spaces… there are pockets of irrational exuberance in the market. It may not be appropriate to allow that froth to keep building.” — Madhabi Puri Buch, Chairperson, SEBI (March 11, 2024)

Imagine this. You have been investing patiently in a small-cap mutual fund for two years. Your portfolio is up 40%. You feel smart. Your WhatsApp group thinks you are a genius.

Then one morning, global markets crash. You open your app. Your ₹8 Lakh is now showing ₹5.2 Lakh. You panic. You tap “Redeem.”

And then — nothing. Your money does not come back in two days. It does not come in a week. The fund house sends you a notice about exit gates and partial payouts. Nobody warned you about this.

This is not a hypothetical horror story. This is the structural reality of small-cap mutual funds in India — and it is exactly why SEBI took a dramatic regulatory step in early 2024.

What you just read is the exact scenario SEBI’s mandatory mutual fund stress test was designed to expose — and prevent.

This article breaks down what the SEBI mutual fund stress test actually means, what the data says about your specific fund, and what you must do right now to protect yourself.

📌 Disclaimer: This article is for educational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully and consult a SEBI-registered financial advisor before making any investment decisions.

“If you want to understand how FII outflows and crude oil shocks amplify small-cap vulnerability, read our complete FII Outflows 2026 breakdown.”

What Is the SEBI Mutual Fund Stress Test?

In February 2024, SEBI and AMFI (Association of Mutual Funds in India) issued a landmark mandate: every AMC running a small-cap or mid-cap fund must publish stress test results once every month (by the 15th of each month). The first historic round of results went live on March 15, 2024, exposing the structural vulnerability of these high-flying portfolios to the general public.

The core question the stress test answers is brutally simple:

If a large chunk of investors suddenly rush for the exit, how many days will it take the fund manager to actually liquidate the portfolio and pay everyone back?

Two specific metrics are measured:

- Days to liquidate 25% of the portfolio

- Days to liquidate 50% of the portfolio

One important nuance worth knowing: SEBI’s methodology allows AMCs to exclude the bottom 20% of the least liquid assets from the stress test calculation. The logic is that in a real redemption crisis, no sensible fund manager liquidates their worst micro-cap positions first — they sell the most liquid holdings available. This exclusion makes the test more realistic, but it also means the actual stress on the remaining 20% is, in effect, a hidden risk layer that these published numbers do not fully capture.

- SEBI’s official stress test circular — https://www.sebi.gov.in/legal/circulars/feb-2024/stress-testing-of-open-ended-mutual-fund-schemes_79988.html

- AMFI’s stress test disclosure portal — https://www.amfiindia.com/stress-test

Why does this matter? Because small-cap stocks — by definition — trade in low volumes on Indian exchanges. On any given day, there may simply not be enough buyers for a fund manager trying to sell large quantities. The fund is, structurally, illiquid.

SEBI is not doing this because they enjoy creating paperwork. They are doing it because ₹40,000+ Crore of retail money flooded into small-cap funds in 2023 alone — and a significant portion of that money belongs to first-time investors who have no idea what they have actually signed up for.

The Inflow Avalanche: How We Got Here

Between 2023 and 2024, Indian markets witnessed a retail investing boom unlike anything before. The numbers tell the story:

- Small-cap mutual funds received over ₹40,000 Crore in net inflows during 2023

- Mid-cap mutual funds absorbed approximately ₹23,000 Crore in the same period

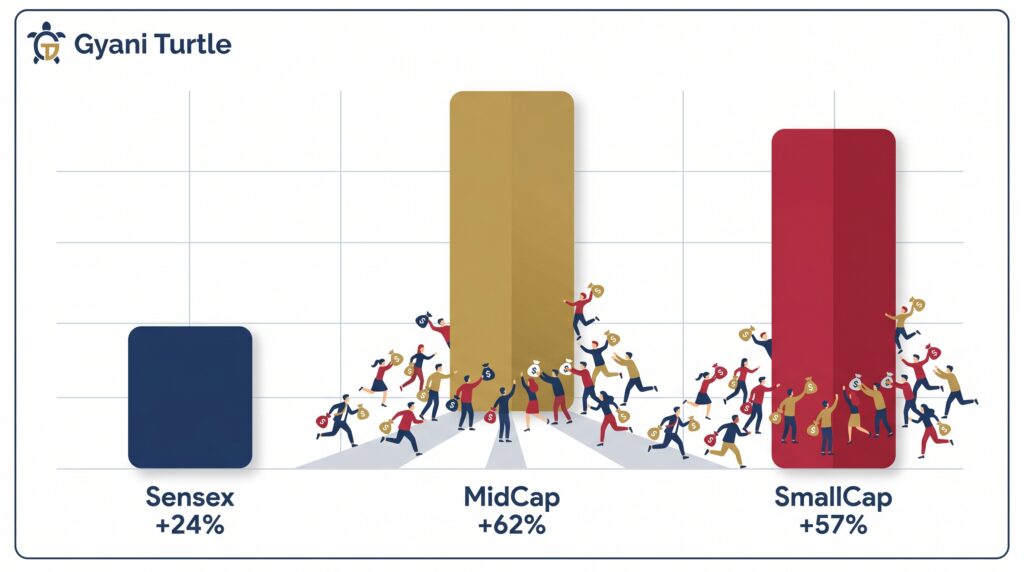

Fuelling this frenzy were eye-popping index returns:

- The BSE MidCap Index surged ~62% in the 2023-2024 period

- The BSE SmallCap Index gained ~57%

- Meanwhile, the large-cap Sensex crawled at just ~24%

The result? Millions of retail investors, many of them first-timers, chased the trailing returns — pumping billions into funds that were simultaneously growing beyond their capacity to manage exits cleanly.

SEBI’s mandate was a direct response to this dangerous mismatch between the size of these funds and the underlying liquidity of the stocks they hold. As one analysis from PersonalFN captured it well: AMCs had shifted from being asset managers focused on sound portfolio construction to asset gatherers — constantly attracting inflows that sometimes exceeded their optimal capacity, without building adequate exit infrastructure.

SEBI Stress Test Data: The Numbers Are Alarming

Here is where it gets real.

For the top 10 largest small-cap funds in India, the average time to liquidate 50% of their portfolio has grown from 29 days in February 2024 to 37 days by January 2025. In less than one year, the average liquidity buffer shrank by a full 8 days.

And one fund stands in a category of its own.

Take Quant Small Cap Fund — initially, its aggressive trading model allowed it to boast a nimble 22 days to liquidate half its assets in early 2024. But as market pressures built and the asset pool warped, that timeline ballooned to 63 days in subsequent 2025 stress cycles. When a fund’s exit door shrinks that fast, it is a silent alarm screaming that the structural liquidity space is running out.

- NSE official shareholding data — https://www.nseindia.com

- AMFI monthly fund factsheet page — https://www.amfiindia.com/net-asset-value

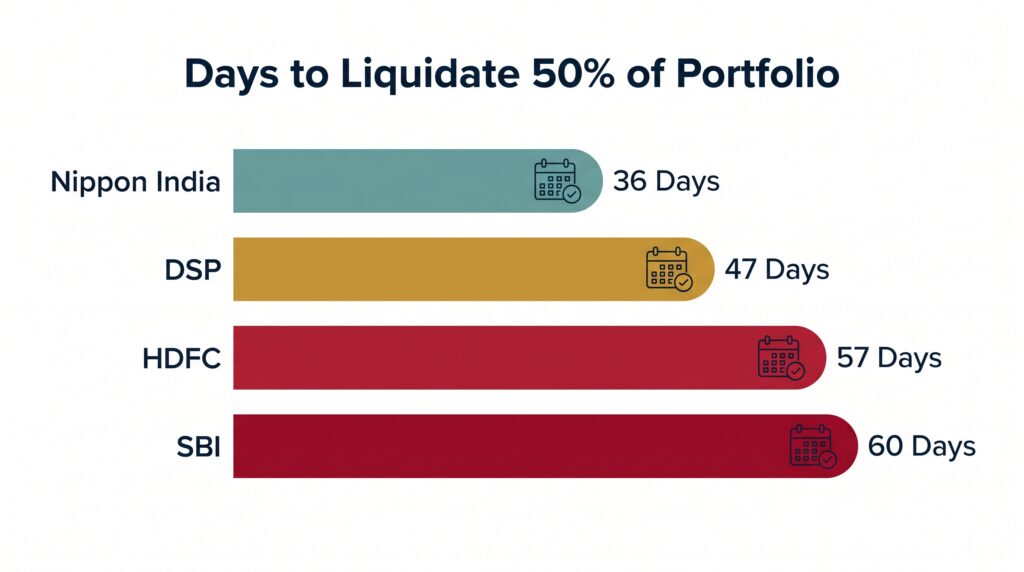

Where Do India’s Biggest Small-Cap Funds Stand Today?

Here is the latest data from AMC disclosures for the heavyweights:

|

Fund Name |

Days to Liquidate 25% |

Days to Liquidate 50% |

|---|---|---|

|

Nippon India Small Cap Fund |

19 days |

38 days |

|

DSP Small Cap Fund |

25 days |

49 days |

|

HDFC Small Cap Fund |

28 days |

55 days |

|

SBI Small Cap Fund |

30 days |

60 days |

Source: AMC Factsheet Disclosures / AMFI, 2025

Let that sink in. If you invest in the SBI Small Cap Fund and a market crisis hits tomorrow, it may take the fund manager up to 60 days to liquidate just half the portfolio in an orderly manner — without devastating the stock prices in the process.

Your EMI does not pause for 60 days. Your child’s school fee does not pause for 60 days. Your emergency does not check the fund’s liquidity calendar.

The Chain Reaction Nobody Tells You About

The real danger of illiquid small-cap funds is not just the investor who loses money. It is the cascade effect that rolls from your app screen all the way to a factory worker being laid off in another city.

Here is exactly how the domino effect works:

Step 1 — The Macro Trigger: High global inflation or a geopolitical shock causes foreign institutions and domestic players to start selling Indian equities.

Step 2 — The Retail Stampede: Ordinary investors, watching daily red numbers on their apps, panic and flood their fund apps with redemption requests.

Step 3 — The Portfolio Trap: Fund managers face billions in exit requests, but small-cap stocks have no buyers. The market simply does not have the depth to absorb large sell orders.

Step 4 — The Forced Fire Sale: To meet redemptions, fund managers are forced to sell their most liquid holdings — large-cap and blue-chip stocks — at whatever price the market will offer.

Step 5 — The Broad Market Collapse: The dumping of blue-chip stocks crashes the Nifty and Sensex. India’s headline indices fall hard. Corporate India’s valuation vaporises on screens worldwide.

Step 6 — The Economic Chokehold: As corporate valuations crash, banks tighten credit lines. Borrowing costs spike. Businesses that were running on working capital debt face a severe cash crunch.

Step 7 — The Micro Impact on Everyday Indians: To protect margins, businesses freeze hiring and cut jobs. Banks raise retail EMIs. The cost of borrowing for a home loan or a two-wheeler goes up. Household budgets tighten. And suddenly, the price of basic essentials feels twice as heavy.

This chain reaction is not theoretical. India saw echoes of it during the 2018 IL&FS crisis. The SEBI stress test is an attempt to prevent the next, much larger version of this spiral. While SEBI’s guardrails are designed precisely to prevent this extreme worst-case scenario, understanding the mechanics of a liquidity trap shows exactly why the regulator is stepping in now.

A Real-World Story: The Sharma Family

Rajesh Sharma (42) is an IT administrator in Noida earning ₹1.2 Lakh per month. He has ₹8 Lakh saved for his daughter’s college education — four years away.

In late 2023, watching colleagues brag about 45% annual returns, Rajesh decides to invest.

The Wrong Path

Rajesh dumps the entire ₹8 Lakh as a lump sum into a top-performing small-cap fund. “Historical charts show it beats everything,” he tells himself. He ignores the SEBI stress test warnings.

A severe market correction hits. His ₹8 Lakh crumbles to ₹5.2 Lakh in three weeks. Panicked, he hits “Redeem.”

Because thousands of others are doing the same, the fund faces a massive liquidity bottleneck. It takes them 50+ days to exit their micro-cap holdings without wiping out the prices further. Rajesh receives chunks at heavily depressed prices. His daughter’s education fund is permanently fractured. He locks in catastrophic losses from which recovery — even with time — is not guaranteed.

The Right Path

Rajesh reads the Gyani Turtle analysis on SEBI’s stress tests. He understands: small-caps are powerful wealth builders over 10+ years, but they are structural traps when the timeline is short and the panic is real.

He reallocates his daughter’s education fund — with its fixed 4-year deadline — into a combination of large-cap index funds and multi-asset allocations, prioritizing liquidity and predictability over high returns.

For his retirement goal (18 years away), he sets up a ₹15,000/month SIP in a mid/small-cap fund. When the market correction hits and liquidity timelines spike, Rajesh does not touch a single rupee. He knows his long horizon shields him. The lower NAV actually buys him more units via rupee-cost averaging. His goals remain intact.

The only difference between these two outcomes is one piece of information, applied at the right time.

How Do Small-Cap Funds Compare to Other Options?

|

Instrument |

Potential Return |

Structural Risk |

Liquidity |

Tax Treatment |

|---|---|---|---|---|

|

Small-Cap Mutual Funds |

High (20–25% long-term potential, highly volatile) |

Extreme — 40–70 day exit bottleneck possible |

Very Low in a panic |

LTCG at 12.5% above ₹1.25 Lakh/year |

|

Large-Cap / Index Funds |

Moderate-Steady (12–14% long-term) |

Low — Liquidated in 1–2 days |

High |

LTCG at 12.5% above ₹1.25 Lakh/year |

|

Fixed Deposits / Debt Funds |

Low (6.5–7.5% nominal) |

Negligible |

Instant |

Taxed at income slab rate |

“Returns are indicative historical averages. Past performance does not guarantee future results.”

Note: Returns are indicative historical averages and not guaranteed. LTCG = Long-Term Capital Gains.

The above table is not an argument against small-cap funds. It is an argument for using them correctly — as a long-horizon, high-conviction allocation, not as a place to park goal-based savings.

What You Must Actually Do Right Now

If You Are a Salaried Investor

1. Audit Your Portfolio Weight. Small-cap mutual fund exposure should not exceed 15–20% of your total equity portfolio unless your investment horizon is 10+ years and you have strong risk tolerance.

2. Stop the Lump-Sum Habit. Never park a large windfall (annual bonus, asset sale proceeds) directly into a small or mid-cap fund. Use a Systematic Transfer Plan (STP) to stagger entry over 6–12 months.

3. Match Horizon to Asset Class. If you need the money within the next 5 years — for a car, a home down payment, education, a wedding — small-caps are generally unsuitable for this timeline. Standard financial planning principles dictate shifting these funds to safer, liquid instruments.

If You Are a Business Owner or MSME Operator

1. Protect Working Capital. Never invest business operational buffers, vendor payment reserves, or advance tax provisioning into mid/small-cap schemes for “extra yield.”

2. Reduce High-Interest Debt Now. When small-cap panic triggers a market selloff, banking credit tightens almost immediately. Clear high-cost business debt while money markets are still liquid.

If You Are an Existing Small-Cap Fund Investor

1. Check the Monthly Disclosures. Go to your AMC’s website or the official AMFI portal by the 15th of every month. Look specifically at the “Days to Liquidate 50% Portfolio” figure. If this timeline is steadily climbing past 45 days, it means the fund manager is getting structurally boxed in. This is a strong signal to re-evaluate your SIP allocations in that specific fund and consult your advisor about pausing fresh inflows.

2. Diversify Across Fund Houses. Do not consolidate all your small-cap SIPs under one large AMC. Spread across multiple fund houses to reduce idiosyncratic fund-level liquidity risk.

“AMC’s website or the official AMFI portal” → https://www.amfiindia.com/stress-test

For Every Indian Family

1. Build Your Emergency Fund First. Keep 6–12 months of core household expenses in liquid instruments — high-yield savings accounts, liquid mutual funds, or overnight funds. This is non-negotiable before any equity investment.

2. Filter Out Social Media Noise. Do not let Instagram reels about small-cap multi-baggers or WhatsApp “tips” dictate where your family’s savings go. Short-term past performance in small-caps is the most misleading data point in personal finance.

The Critical View: Is SEBI’s Stress Test Itself Flawed?

A balanced perspective demands that we present the counterargument, and there are credible ones.

The Tests May Be Overly Alarmist. The stress test assumes that 25% or 50% of investors simultaneously demand their money back. Critics — including seasoned fund managers — point out that in the entire history of Indian mutual funds, a 50% mass redemption in a single event has never actually occurred. The scenario is extreme by design.

A Possible Self-Fulfilling Prophecy. By forcing public disclosure of “60-day liquidation windows,” the regulator may inadvertently trigger the very panic it wants to prevent. A retail investor who sees a 60-day number may redeem early out of fear — initiating the cascade that would not have started otherwise. This is a genuine concern.

Closet Large-Cap Indexing. To improve their stress test scores, some fund managers are reportedly holding cash buffers of 7–10% and tilting their small-cap portfolios towards more liquid large-cap names. This effectively turns your small-cap fund into a diluted, expensive large-cap fund — high fees, lower alpha.

These criticisms do not invalidate SEBI’s intent. But they are important context. The stress test is a measuring instrument, not a guarantee of safety. A thermometer can tell you a patient has a fever; it cannot cure them.

Frequently Asked Questions

Q: Where can I check my fund’s SEBI stress test results?

Go to your AMC’s official website or visit amfiindia.com. Results are published by the 15th of every month under the “Stress Test” or “Portfolio Disclosure” section.

Q: What is a safe number of days in a stress test?

Generally, a 50% liquidation time under 25–30 days is considered healthy. Above 45 days signals meaningful liquidity risk. Above 60 days is a serious structural warning for short-horizon investors.

Q: Does a high stress test number mean I should exit?

Not automatically. If your investment horizon is 10+ years and you invest via SIP, a higher number matters less. If your goal is within 5 years, it matters a lot.

Q: Is the stress test mandatory for large-cap funds?

No. SEBI’s current mandate covers only small-cap and mid-cap schemes. Large-cap funds are exempt because their underlying stocks are significantly more liquid.

Q: How often does SEBI update the stress test rules?

SEBI reviews and updates the methodology periodically. The current framework has been in place since February 2024 with monthly disclosure requirements.

The Gyani Turtle Takeaway

SEBI’s fortnightly stress test mandate is one of the most important investor protection measures introduced in Indian markets in the last decade. It is also widely misunderstood and largely ignored by the retail investors who need it most.

Here is the patient investor’s summary:

✅ Small-cap funds are not evil. Over long horizons with disciplined SIPs, they remain one of the best wealth-creation vehicles in India.

✅ The stress test is a tool, not a verdict. Use it the same way you check tyre pressure before a long drive — not because you expect a blowout, but because you deserve to know the risk you are carrying.

✅ The danger is not the fund — it is the mismatch. Wrong money (short-horizon, goal-based) in the wrong vehicle (illiquid small-cap) is where the real damage happens.

✅ Check the numbers every 15 days. AMFI publishes them. Your AMC publishes them. There is no excuse for not looking.

The market will correct again. It always does. The investors who survive and thrive are not the ones who picked the best fund — they are the ones who understood the risks, structured their portfolio accordingly, and stayed calm when everyone else panicked.

Invest like a patient investor.

Key Data Quick Reference

|

Metric |

Value |

Source |

|---|---|---|

|

Stress test reporting frequency |

Once every month (by the 15th) |

SEBI/AMFI Directive |

|

First disclosure date |

March 15, 2024 |

AMFI |

|

2023 Small-Cap net inflows |

Over ₹40,000 Crore |

AMFI Industry Report, Jan 2024 |

|

2023 Mid-Cap net inflows |

~₹23,000 Crore |

AMFI Industry Report, Jan 2024 |

|

Top 10 funds avg. 50% liquidation (Feb 2024) |

29 days |

Business Standard |

|

Top 10 funds avg. 50% liquidation (Mid-2026) |

~40 days |

AMFI / Industry Estimates |

|

Quant Small Cap 50% liquidation |

~60 days |

AMFI / AMC Disclosure, May 2026 |

|

SBI Small Cap 50% liquidation |

~60 days |

AMFI / AMC Disclosure, May 2026 |

|

HDFC Small Cap 50% liquidation |

57 days |

AMFI/AMC Disclosure, 2025 |

|

DSP Small Cap 50% liquidation |

47 days |

AMFI/AMC Disclosure, 2025 |

|

Nippon India Small Cap 50% liquidation |

36 days |

AMFI/AMC Disclosure, 2025 |

|

BSE MidCap Index 1-yr gain (2023-24) |

~62% |

Economic Times |

|

BSE SmallCap Index 1-yr gain (2023-24) |

~57% |

Economic Times |

“Source: AMC Factsheet Disclosures / AMFI 2025. Data is indicative and subject to change monthly.”

📌 The data points referenced in this article are sourced from SEBI circulars, AMFI industry disclosures, Business Standard, and Economic Times reports. All information is for educational purposes only. Please verify the latest stress test disclosures directly on your AMC’s website or AMFI’s portal before making any investment decision.

Also Read on Gyani Turtle:

- Market Volatility Reasons India: 3 Reasons Not to Panic

- FII Outflows India 2026: What Record Foreign Selling Means for Your Portfolio, EMIs, and Savings

- Large-Cap vs Small-Cap: Why ‘Quality’ Matters in 2026

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before making investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.