Should Indian Investors Invest in China’s Stock Market in 2026?

In investing, the best opportunities rarely come wrapped in good news. If you’re wondering whether to invest in China from India in 2026, this post answers that question with data — not hype, not fear.

They come wrapped in geopolitical tension, regulatory uncertainty, and a general consensus that the asset in question is either dead or dying. That is precisely the situation with invest in China — specifically Chinese equities — in 2026.

The mainstream narrative is familiar: China’s property sector is a slow-motion collapse, the US–China trade war under Trump 2.0 is escalating, demographic headwinds are worsening, and Beijing’s regulatory hand remains unpredictable. Every month brings a fresh reason to stay away.

And yet — quietly, without fanfare — Chinese markets are having a remarkable year.

The Shanghai Composite has climbed to 4,180 points as of May 7, 2026 — up nearly 25% year-on-year. The Hang Seng Index in Hong Kong has pushed to 26,600+, its highest level since February 2026. Global institutional investors, after years of underweighting China, are quietly choosing to invest in China again.

More Indian investors are asking whether to invest in China in 2026 than at any point in the last five years.

So the contrarian question must be asked: Is this the moment for patient Indian investors to invest in China — or is it still a value trap dressed as an opportunity?

That is what this post will answer. Not with hype, not with fear. With data, structure, and the Gyani Turtle lens.

The Contrarian’s Dilemma: China’s Market in May 2026

Let us start with what the markets are actually doing — because most headlines are still stuck in the doom narrative of 2023–2024.

China’s Shanghai Composite rose to 4,180 points on May 7, 2026, gaining nearly 25% compared to the same time last year. The broader Shenzhen Component has been even stronger — climbing to over 15,460, its strongest reading since February 2021.

In Hong Kong, the Hang Seng Index closed up 1.6% to reach 26,626 points on May 7 — its highest level since February 2026 — with gains driven by easing geopolitical tensions and strong technology-sector buying.

What is driving this recovery? Three factors are working together:

China’s domestic AI and semiconductor push.

With US export restrictions on advanced chips forcing China to build its own technology ecosystem, domestic semiconductor and AI infrastructure companies have been the standout performers of 2026. The CSI 300, which tracks the top 300 stocks across both Shanghai and Shenzhen, hit 4,877 points this week — representing a remarkable 27.5% increase compared to a year ago. A key catalyst: DeepSeek’s V4 model launched in February 2026 around the Lunar New Year, and by May 2026, markets are now processing an entire quarter of real-world implementation data showing its efficiency running on domestic Chinese silicon — a powerful proof point for China’s tech self-reliance thesis.

Beijing’s stimulus floor.

The People’s Bank of China has deployed significant monetary easing and fiscal stimulus, effectively placing a policy floor under the collapsing property sector and stabilising consumer confidence. Official manufacturing PMI data beat market expectations at 50.3 in April 2026, while a private survey showed manufacturing PMI climbing to its highest level since December 2020 at 52.2.

Geopolitical easing.

The US–Iran conflict, which had rattled global markets since February 2026, appears to be moving toward de-escalation — lifting sentiment across Asian markets broadly.

China is no longer the hyper-growth engine of 2010. It is a massive, restructuring economy pivoting from real estate to deep technology. And until recently, it was pricing in maximum pessimism — which is precisely when patient investors pay attention.

The Valuation Game: Is China Actually Cheap?

The first question a value investor asks is always the same: what am I paying for earnings?

The case to invest in China becomes harder to ignore when you compare valuations across global markets.

As of early 2026, the Shanghai stock market carries a trailing price-to-earnings ratio of approximately 18x and a forward P/E of around 15x — multiples based on the SSE Composite Index, the primary benchmark for mainland China’s stock market.

Compare that with India’s Nifty 50, currently trading at roughly 21x earnings — a premium that reflects our high growth expectations and political stability. And compare both with the US S&P 500, which has been trading at 24x+ earnings, driven by AI euphoria and a handful of mega-cap technology companies.

The picture is stark:

|

Market |

Index |

Trailing P/E |

YoY Performance |

2026 GDP |

Primary Driver |

|---|---|---|---|---|---|

|

China (Old Economy) |

Shanghai Composite |

~17–18x |

+25% |

4.4% |

Stimulus, SOEs |

|

China (New Economy |

CSI 300 |

~18–19x |

+27.5% |

4.4% |

AI, Tech, EVs |

|

India |

Nifty 50 |

~21x |

~12–15% |

6.5–7.0% |

Domestic demand |

|

USA |

S&P 500 |

24x+ |

~10–12% |

2.0–2.5% |

AI, Mega-cap tech |

Note: The CSI 300 is the better lens for understanding “New China” — it captures the AI, EV, and semiconductor companies driving the recovery, versus the Shanghai Composite which is dominated by older state-owned banks and industrial firms.

China is objectively the cheapest of the three major markets by this measure. But a low P/E is only attractive if the earnings are sustainable — and in China, earnings are heavily influenced by government policy. Which brings us to the risks.

The Gyani Turtle Read: Cheap alone is never enough. The question is whether cheap is cheap for a reason that is permanent — or cheap because the market is pricing in fear that is temporary. The answer determines everything.

The Big Three Risks: What Could Go Wrong

Before deciding to invest in China, every patient investor must stare at three risks directly.

Risk 1 — The US–China Trade War

Trump 2.0 has been aggressive on trade. The most consequential legal battleground right now is Section 122 — a 10% global baseline tariff that is currently being challenged in the US Supreme Court. If upheld, it further chokes Chinese export competitiveness across every sector, not just steel and aluminium. Beyond Section 122, targeted tariffs on Chinese manufactured goods have escalated significantly, with the clear intent to decouple American supply chains from Chinese manufacturing. For Chinese export-heavy companies, this is a structural headwind — not a temporary one.

Risk 2 — Regulatory Whiplash

This is the risk that separates China from every other market. In 2021, the Chinese Communist Party wiped out hundreds of billions in shareholder value virtually overnight — cracking down on Alibaba, Didi, and the entire EdTech sector in the name of “Common Prosperity.” The state can change the rules of capitalism on a Tuesday morning, without warning, without recourse.

The government’s increased oversight of the private sector — particularly in tech, education, and financial services — has dampened earnings potential, and public companies may not fully reflect the broader economy’s performance due to the dominance of state-owned enterprises that often prioritise government goals over profit maximisation.

Beijing has softened its stance in 2026 to lure back foreign capital. But the trauma of 2021 is not forgotten — and it should not be.

Risk 3 — The Taiwan Geopolitical Premium

Markets price uncertainty with a permanent discount. The ever-present possibility of cross-strait conflict with Taiwan acts as a ceiling on how enthusiastically global capital will embrace Chinese equities. If conflict were to break out, Western sanctions could freeze foreign investments overnight — as happened with Russian equities in 2022.

This is not a probability assessment. It is a tail risk that must be sized for in any position.

The Opportunity Case: Why Global Funds Are Quietly Returning

If the risks are so significant, why are institutional investors — cautiously but unmistakably — coming back to invest in China?

The Tech Self-Reliance Boom

US chip export restrictions have had an unintended consequence: they have forced China to accelerate its domestic semiconductor and AI ecosystem faster than anyone expected. Companies like SMIC, Cambricon, and Hygon are attracting massive state-backed investment, and early results have surprised even sceptical Western analysts. With less regulatory oversight on China’s tech industries, a sustained rebound could mean that the Hang Seng has plenty of room to run as its low-cost AI leaders continue to win admirers around the world.

The GDP Reality Check

China’s GDP growth of 4.4% in 2026 sounds modest compared to India’s 6.5–7%. But consider the base: China’s current annual GDP stands at approximately $20,479 billion USD. A 4.4% growth rate on an $18–20 trillion economy creates an enormous amount of absolute wealth — more, in absolute dollar terms, than India’s faster-growing but smaller economy.

Mean Reversion

Markets move in cycles. After years of Chinese underperformance relative to US and Indian equities, global asset managers are rebalancing. They are locking in profits from expensive US tech positions and choosing to invest in China across manufacturing, consumer, and technology stocks as a portfolio hedge. The offshore Hong Kong market has notably outperformed the onshore market, reflecting international investors’ growing appetite to invest in China, with real estate, materials, and industrials emerging as the new sector leadership — a broadening of the rally that signals healthy market development rather than narrow, momentum-driven gains.

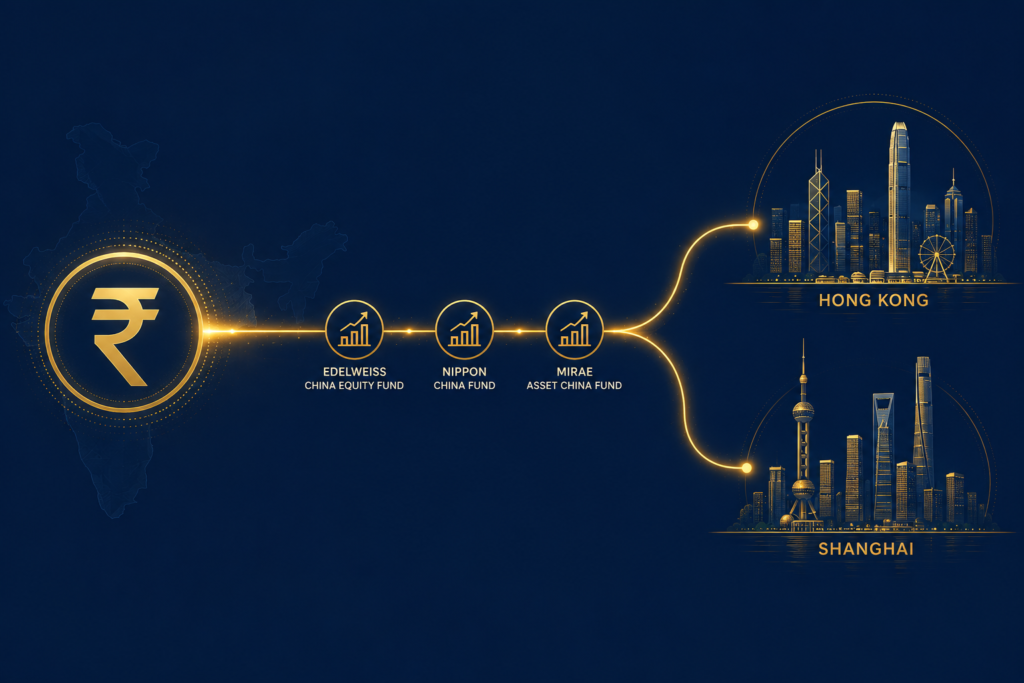

How to Invest in China from India in 2026 — Your Practical Options

This is where most blogs stop — and where the Gyani Turtle goes deeper. Because wanting to invest in China and actually getting it from India are two different things.

The SEBI Constraint

SEBI has historically capped the mutual fund industry’s aggregate overseas investment at $7 billion USD. Individual fund houses operate within sub-limits of this cap. As of May 2026, several funds — including Edelweiss and Invesco — are currently accepting fresh SIPs, as redemptions in other global funds have created headroom within the industry limit. However, this window can close quickly. Always verify availability directly on the AMC website or Value Research before investing.

Your Practical Options

Edelweiss Greater China Equity Off-shore Fund — The standout performer among India-domiciled China funds. As of May 5, 2026, it carries an AUM of ₹2,678.3 Crore with a current NAV of ₹66.05 (Regular Growth). Its 1-year return of approximately 73.2% — against a category average of roughly 23% — reflects its heavy weighting in the semiconductor and AI recovery stocks that led China’s market rebound. It operates as a feeder fund into JPMorgan’s Greater China strategy, giving exposure to Hong Kong-listed companies including Alibaba, Tencent, and Meituan. As of this writing, SIPs and lump-sum investments are currently being accepted due to headroom created by recent redemptions in other global funds — but this can change without notice.

For those looking to invest in China from India in 2026, here are your practical regulated options. There are three regulated ways to invest in China from India right now.

Nippon India Taiwan Equity Fund —

While technically Taiwan-focused, this fund provides significant exposure to the broader Greater China semiconductor and hardware supply chain — relevant given the AI infrastructure buildout across the region.

Mirae Asset China Fund —

Another feeder fund structure providing access to Chinese equities. Check current SIP and lump-sum availability with your broker.

One critical rule:

Always verify with your broker or the AMC directly whether fresh SIPs are currently accepted. Fund houses frequently pause and resume these schemes based on SEBI’s daily limit tracking. What was open last month may be closed today — and vice versa.

The Indirect Route —

For investors who want broad exposure without the complexity of single-country China funds, global emerging market ETFs — an indirect way to invest in China from India — and Nasdaq 100 FOFs like Motilal Oswal’s — give indirect exposure to the broader Asia technology buildout, though China weight varies by fund.

The India–China Political Angle: Pragmatic Decoupling

The question every Indian investor carries is personal — not just financial.

Post-Galwan 2020, the trust deficit between New Delhi and Beijing remains real and deep. Nationalist sentiment runs high. The border stand-off is unresolved. The decision to invest in China can feel, to some Indian readers, like a moral question — not just a financial one.

The Gyani Turtle’s position: this is your money, your decision, and your values. We will not tell you what to feel about it.

What we will tell you is the regulatory reality: your decision to invest in China through mutual funds is completely legal, fully SEBI-regulated, and entirely separate from border politics. The Indian government has itself made pragmatic moves — the DPIIT revised FDI policy in early 2026 to allow overseas companies with up to 10% Chinese shareholding to invest via the automatic route, provided the investing entity itself is not based in a country sharing a land border with India. This nuanced distinction signals that economic pragmatism and geopolitical caution can coexist — and that New Delhi is making room for capital flows while maintaining strategic guardrails.

Both nations are practicing “pragmatic decoupling” — which means Indians can invest in China legally and safely within SEBI’s framework — competing fiercely on borders and in global supply chains, while maintaining the economic channels necessary for regional stability. As an investor, you operate within the legal framework. What you do within it is a personal call.

What Should Indian Investors Actually Do?

Here is the Gyani Turtle verdict — structured, honest, and sized for reality.

Who Should NOT Invest in China:

The Anxious Investor. If headlines about trade wars, regulatory crackdowns, or Taiwan tensions will cause you to panic-sell at the worst possible time — stay away. China is not a market for people who watch the news every morning and react to it. Volatility here is not a bug. It is a feature.

The Short-Term Trader. To invest in China is to bet on a structural turnaround story. If your time horizon is under five years, this market will likely frustrate you more than it rewards you. The recovery is real but uneven. Patience is the non-negotiable entry requirement.

Who Should Consider It — And How:

The Contrarian Value Investor. If you understand that buying low means buying when sentiment is terrible — and you have the temperament to hold through volatility — to invest in China offers one of the most compelling valuation gaps in global equities today. A market where you invest in China at 17–18x earnings while it grows at 4.4% on a $20 trillion base is not obviously cheap. It is structurally cheap.

The 3–5% Satellite Rule. China should never be the core of an Indian investor’s equity portfolio. It is a satellite position — meaningful enough to matter if the recovery plays out, small enough that a geopolitical black swan does not derail your financial independence. A 3% to 5% allocation of your total equity portfolio to a Greater China mutual fund is the range that makes mathematical sense for most investors.

The Milestones to Watch:

- Mid-2026: Release of any new SEBI overseas investment limit revision — this determines availability of China funds in India

- Late 2026: US–China trade war trajectory under Trump’s second term — any de-escalation would be a significant catalyst

- 2026–2027: Whether China’s domestic AI and semiconductor companies deliver on their promise at scale

The Gyani Turtle Verdict

China in 2026 is not an easy bet. It has never been an easy bet.

The decision to invest in China from India in 2026 comes down to three things: temperament, time horizon, and position sizing.

The property sector is still structurally weak. The regulatory environment remains opaque by global standards. The US–China trade war is a genuine headwind for exporters. And the Taiwan risk, however low its probability, carries asymmetric consequences.

And yet. A market trading at 17–18x earnings, growing at 4.4% on a $20 trillion base, with a domestic technology sector that has surprised sceptics and a government that has clearly decided it will not allow equities to collapse — is not a market to ignore entirely.

The question is not whether to invest in China at all. The question is whether you have the temperament, the time horizon, and the position sizing discipline to hold it through the inevitable moments when the headlines turn dark again.

If yes — a 3–5% satellite allocation, deployed systematically — the smartest way to invest in China from India through a regulated mutual fund, is a rational choice for a patient investor with a five-year horizon.

If no — there is no shame in that answer. Great investing is as much about knowing your own psychology as knowing the market.

Whether you choose to invest in China or not, the decision must be made with full awareness of both the opportunity and the risks.

Invest patiently. Analyse deeply. React rarely.

That’s the Gyani Turtle way. 🐢

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before making investment decisions.

At Gyani Turtle, we believe every Indian deserves access to honest, jargon-free financial education. Our team simplifies investing, mutual funds, and personal finance — so you can build real wealth, one smart decision at a time. Not SEBI registered. For educational purposes only.

One Comment